We look back at the first quarter of 2022 and the news that shaped it, as well as important events in the future.

QUICK TAKEAWAYS

Bitcoin battles back to nearly flat on the quarter after a tough start. 1Q is typically mixed for price performance.

Interest rates were a headwind in the quarter, but the good news is investors have now priced in a hawkish Fed.

Correlations between bitcoin and equities are at all-time highs.

Russia’s invasion of Ukraine highlights some of the benefits of Bitcoin.

Public crypto companies were down on the quarter, highlighting a growing performance divergence with the price of bitcoin.

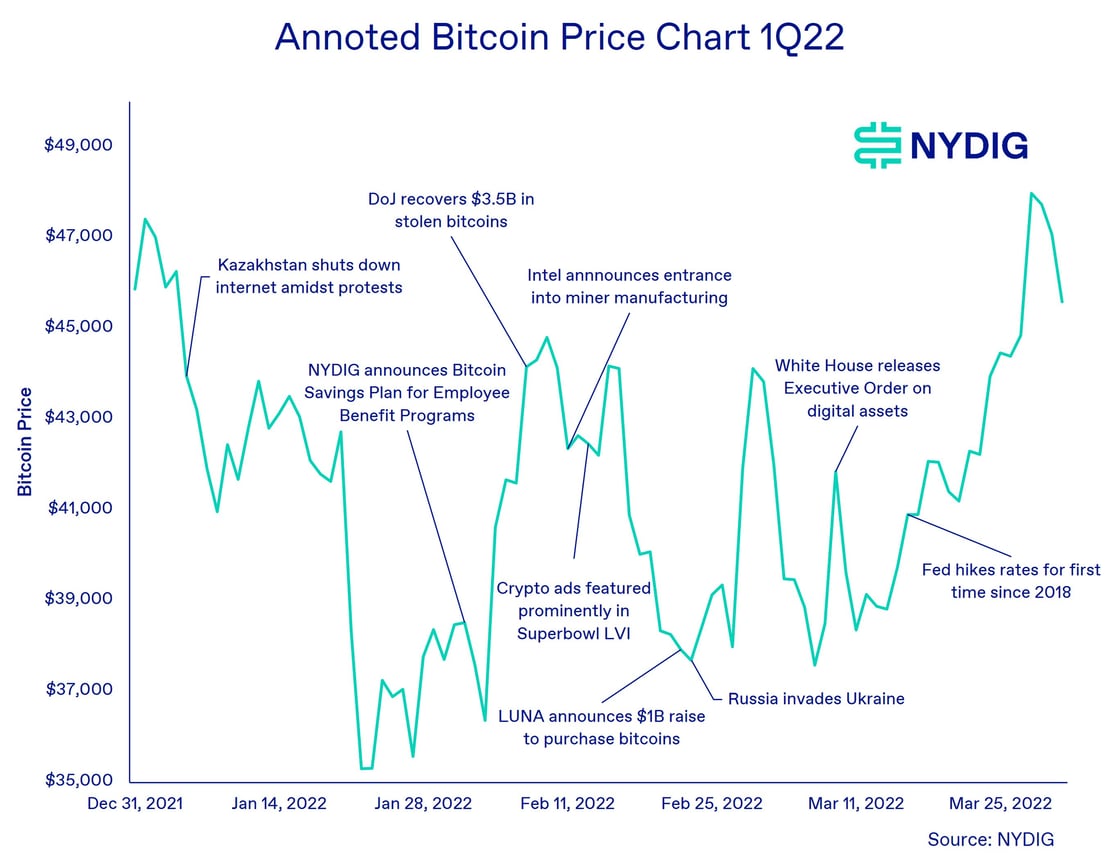

The White House’s executive order strikes a positive note for crypto.

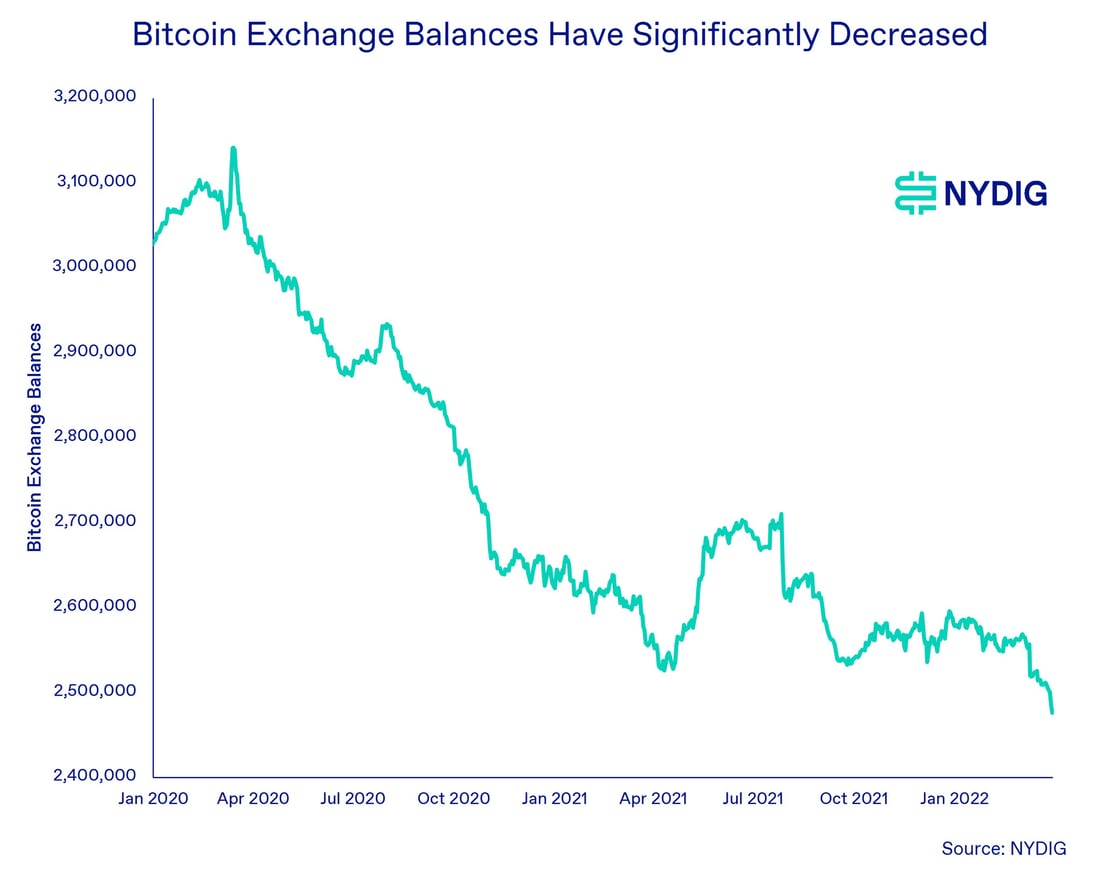

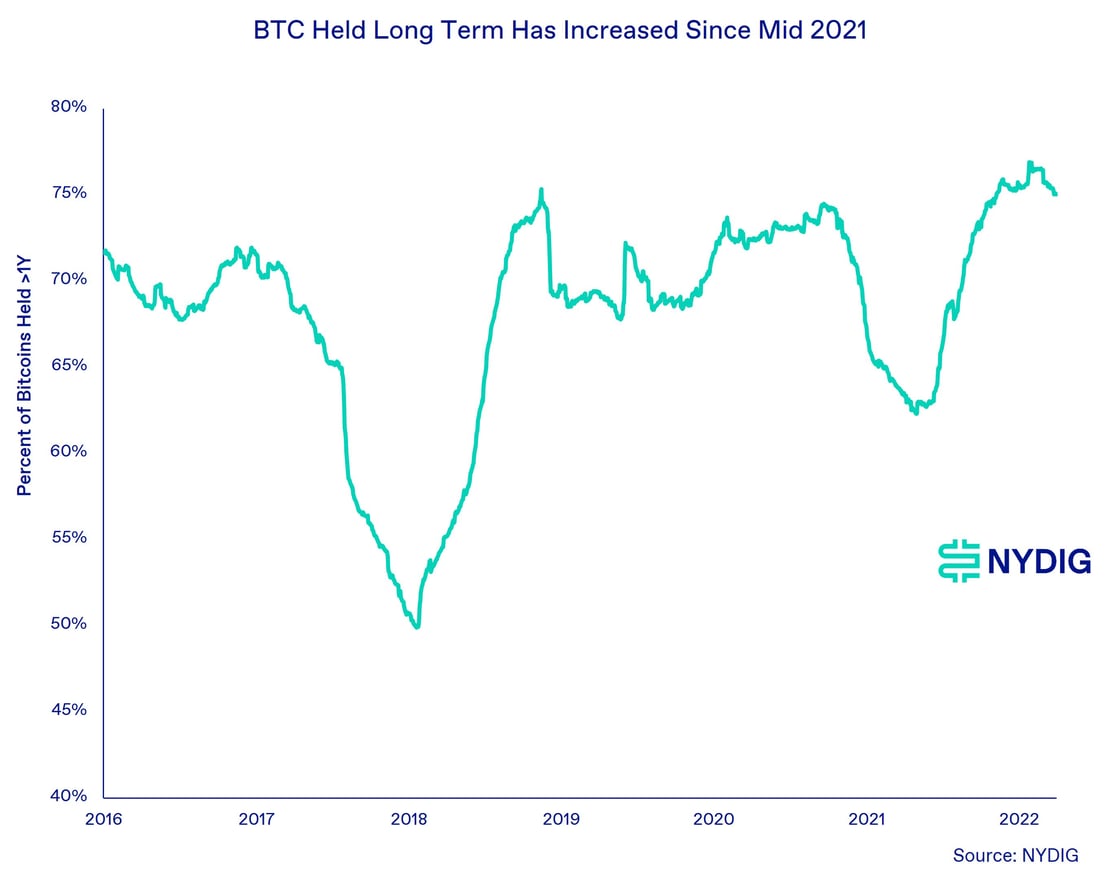

Investors are holding bitcoin for longer and taking them off exchanges.

Bitcoin becomes a stablecoin reserve for the Terra ecosystem.

We take a look at some potential upcoming catalysts, such as the conference circuit and tax season.

PERFORMANCE REVIEW

Bitcoin Bounces Back After a Slow Start

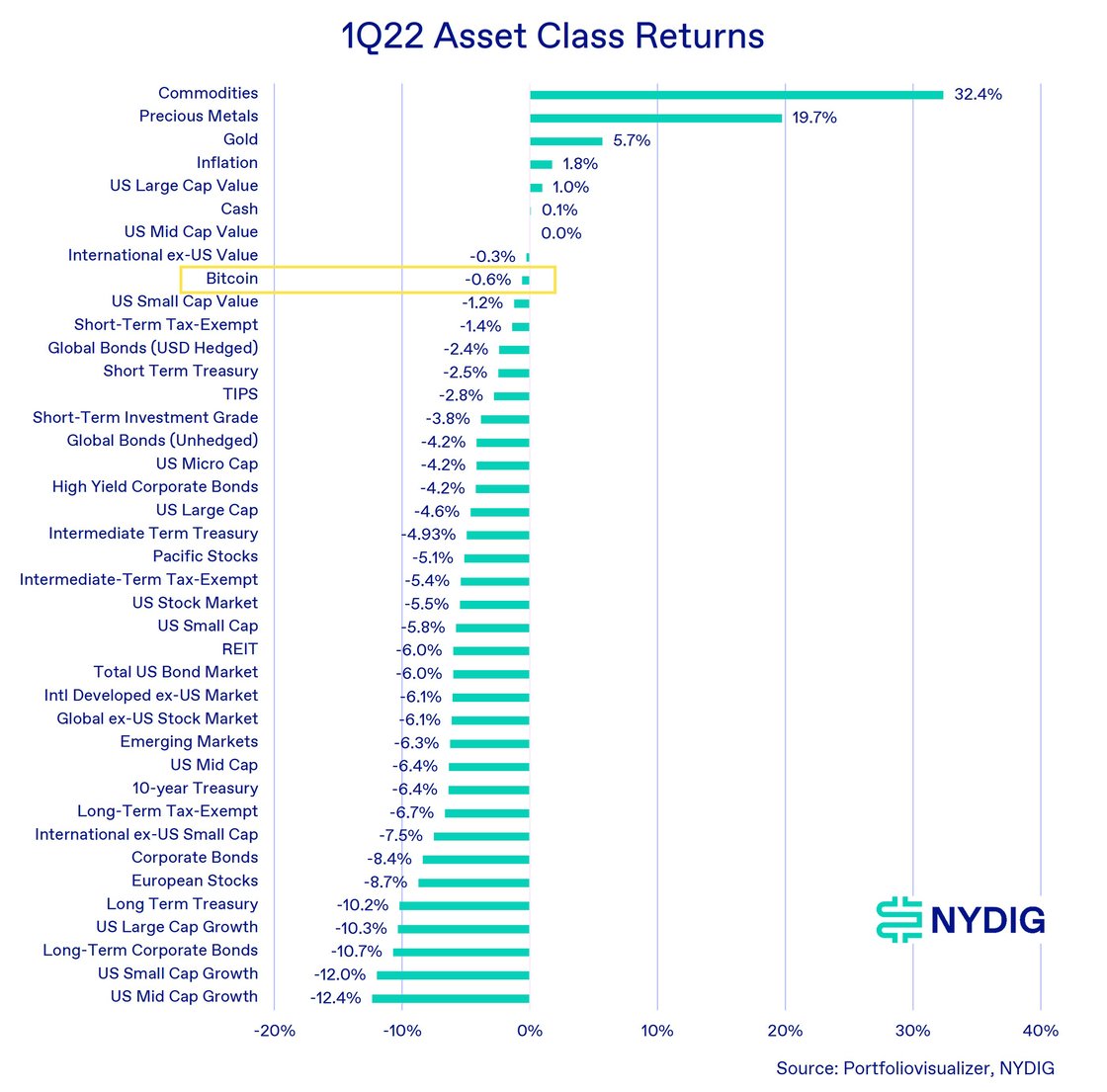

It was a tough start to 2022 for most asset classes. It started with rising interest rate expectations and ended with Russia invading Ukraine. Aside from commodities, many of which benefited from the resulting supply shock caused by international sanctions, most asset classes struggled against that backdrop. In this context, we think bitcoin fared well by comparison.

Alongside equities, bitcoin began the year by continuing its negative price performance from late last year as high inflation numbers seemed to guide a more hawkish stance by the Federal Reserve. Bitcoin’s drawdown, the 6th worst in its history, troughed on January 24 at $32,933.33 (looking at 4 pm ET snapshots). The price recovered from these lows and remained rangebound between roughly $38,000 and $42,000 for much of the rest of the quarter as prices seemed unsure how to react to Russia’s invasion of Ukraine and the geopolitical instability that ensued. Bitcoin then further recovered to $45,595.55 to finish off the quarter, ending down -0.6%.

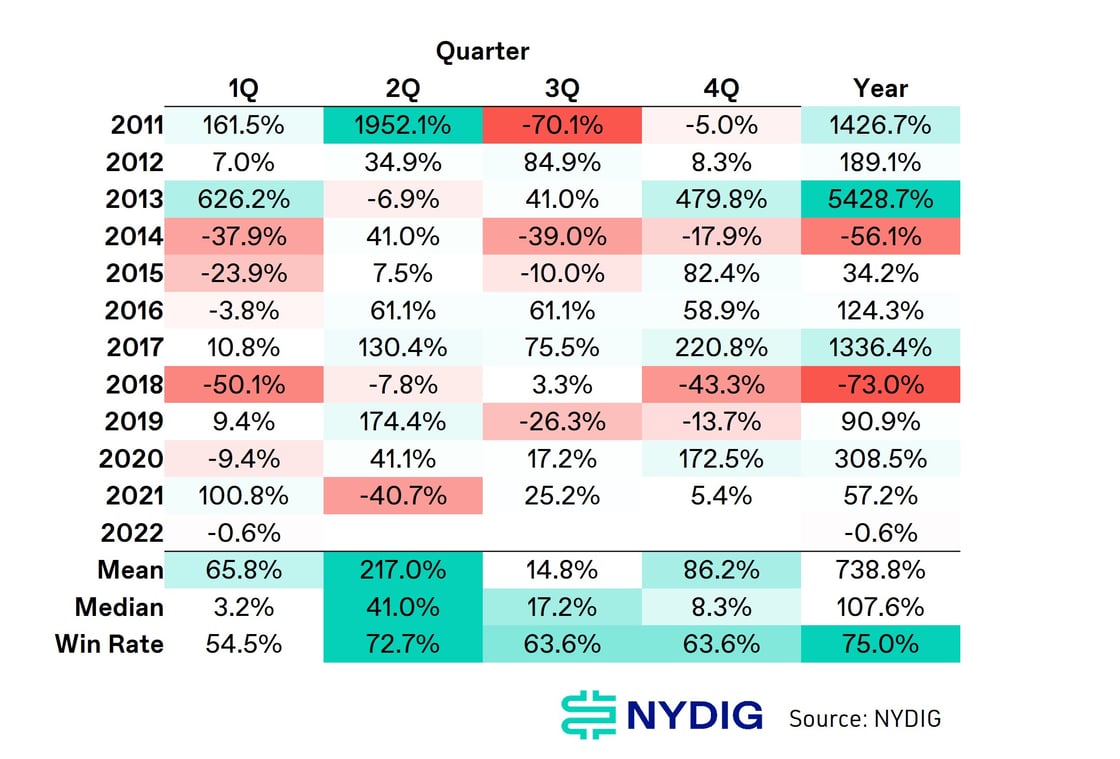

Quarterly Performance In-Line with Mixed Seasonality

The first calendar quarter has typically been mixed for bitcoin from a price-performance standpoint. Its win rate, the percentage of quarters it has exhibited positive performance, was only a little better than half. This is opposed to the second quarter, which has the highest win rate (72.7%) and median return (41.0%). As such, this first quarter was roughly in line with the historical trend.

EVENTS THAT SHAPED THE QUARTER

Interest Rate Fears Cool Markets

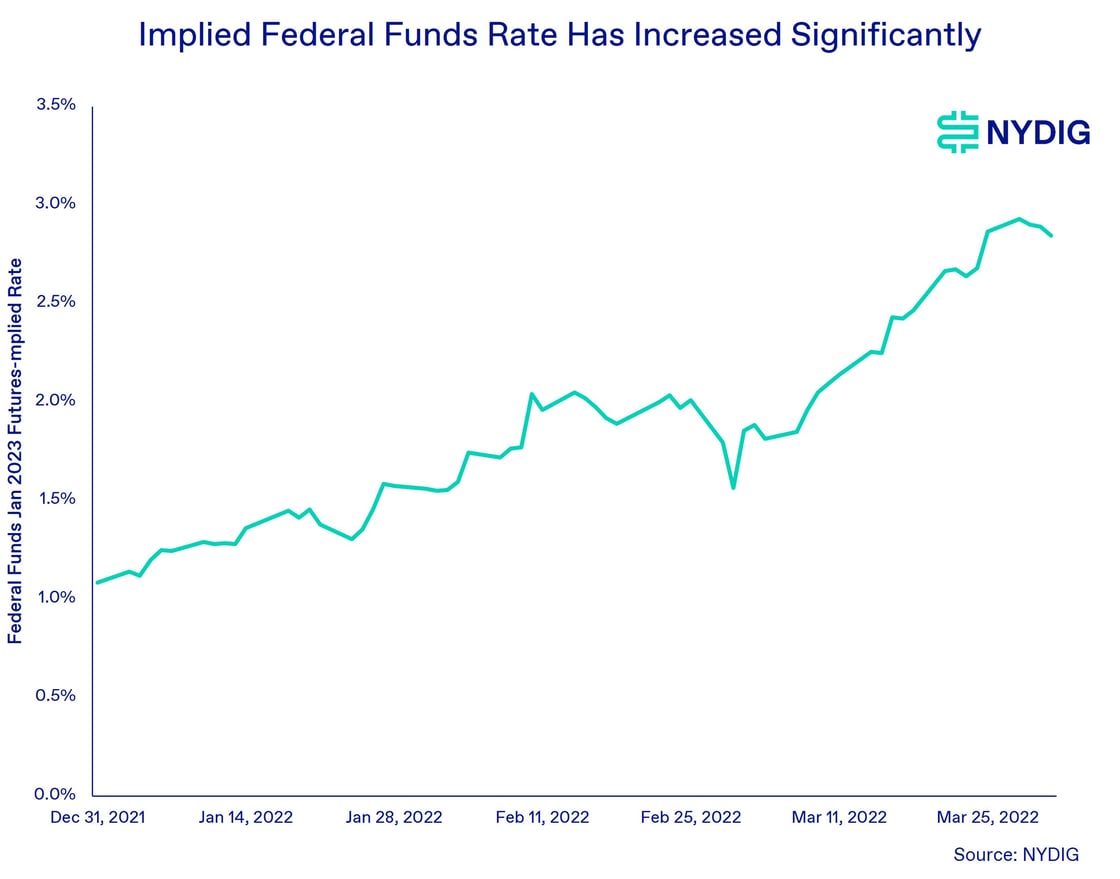

The story coming into the year was the Fed’s signaling for higher interest rates as a mechanism to fight inflation, which, in their eyes, went from “transitory” to something more permanent. In March, the FOMC made good on that pledge, raising the range for the Fed Funds rate by 25 bps. The market is expecting that to just be the tip of the iceberg with more hikes anticipated over the year. The implied rate in 12 months going by the Fed Funds futures market is 2.87%, well above the 0.25 – 0.50% range, and well above implied rates seen just earlier this year.

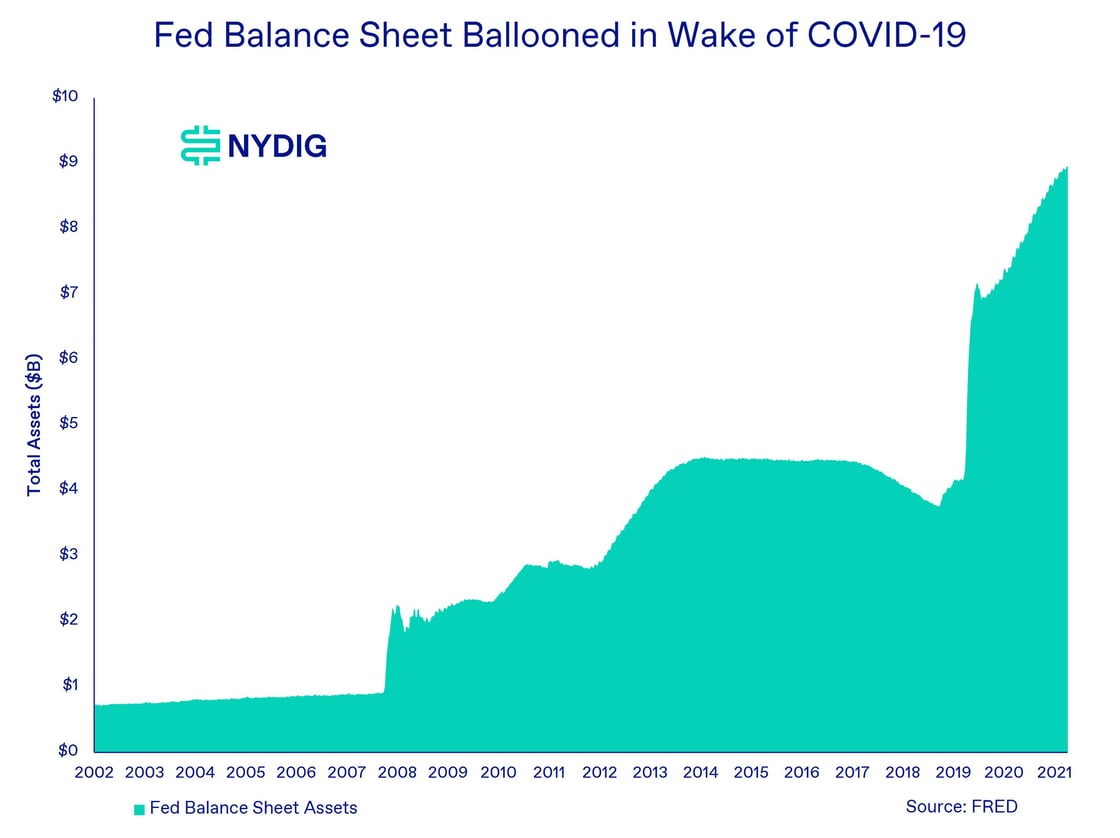

Apart from the pace of rate hikes, one current unknown is how the Fed plans to handle its balance sheet, which has ballooned to nearly $9T of agency debt, mortgage-backed securities, and Treasuries. Roughly half that balance stems from COVID-19 quantitative easing (QE) measures. Investors should be aware that the Fed was never able to fully unwind the QE measures it put in place in the aftermath of the Global Financial Crisis way back in 2007 – 2008. We expect to hear more about balance sheet plans in future FOMC meetings, likely starting on May 4. Hawkish actions would include outright asset sales, while dovish actions would be a balance sheet run-off, by not reinvesting proceeds from coupons and maturing bonds.

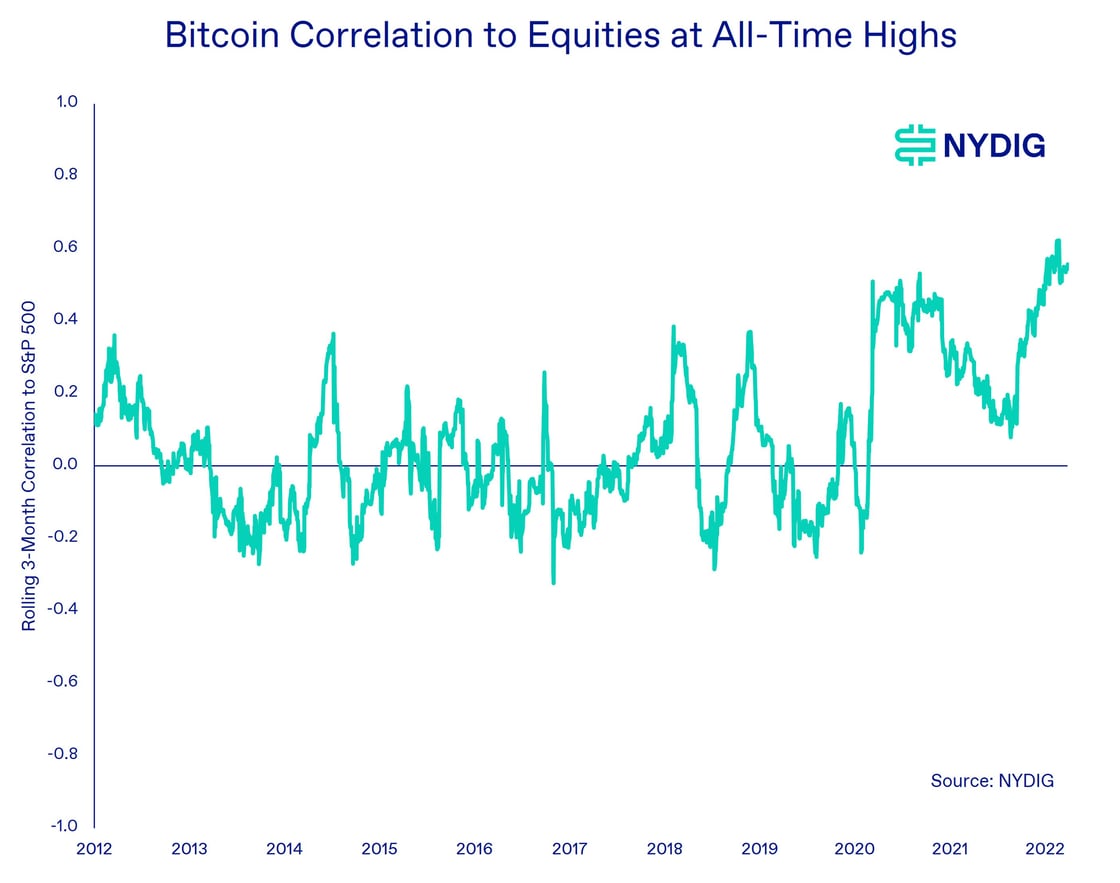

Equity Correlations at All-Time Highs

Since the beginning of the fiscal and monetary response to COVID-19 in March 2020, the rolling quarterly correlation between bitcoin and risk-on assets, such as US equities, has remained consistently positive, reaching its highest level ever at just over 0.6.

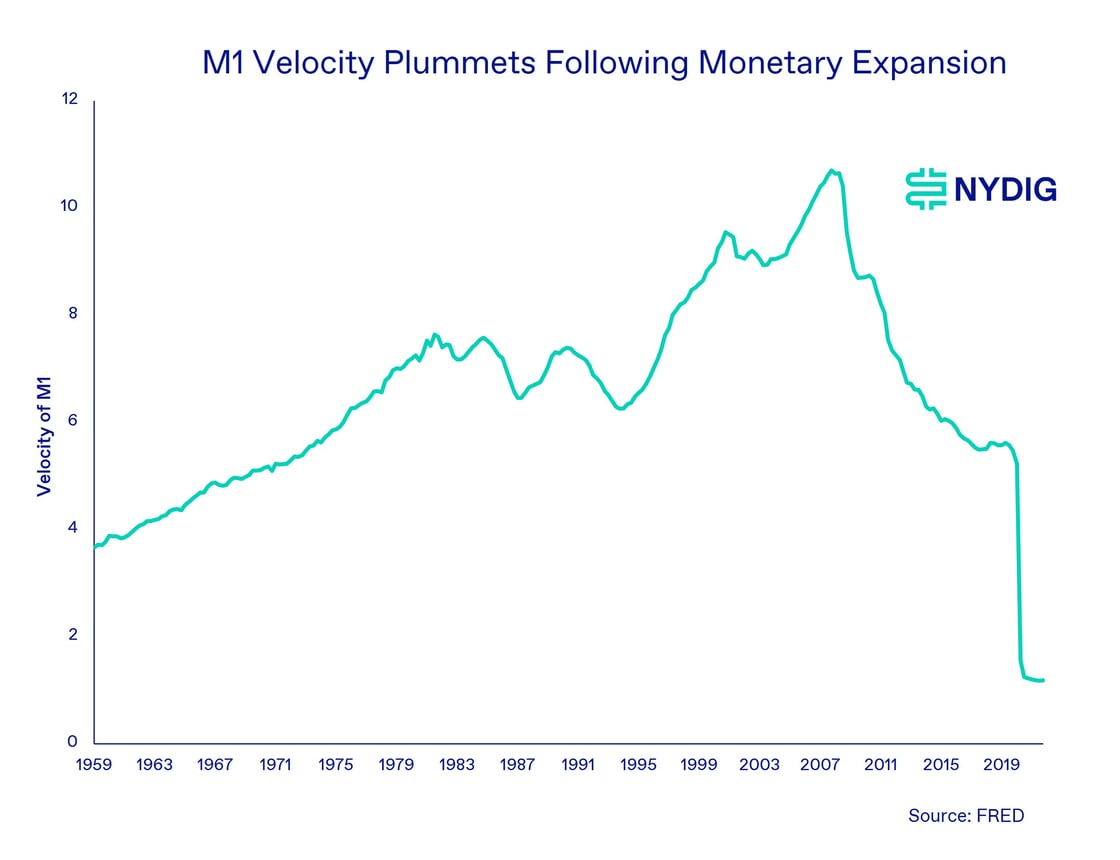

One reason for the rising correlations may be monetary stimulus. Equities and bitcoin do not share fundamental factors. However, the two asset classes were beneficiaries of the global liquidity created by monetary and fiscal stimulus created in response to COVID-19. That effect is demonstrated by the declining velocity of the money supply, which shows that money from the stimulus, by and large, did not go into the economy. Now that those supportive measures are being reversed to combat inflation, it is taking global liquidity out of all corners of financial markets. That’s proving to be a drag on asset prices in digital and equity markets.

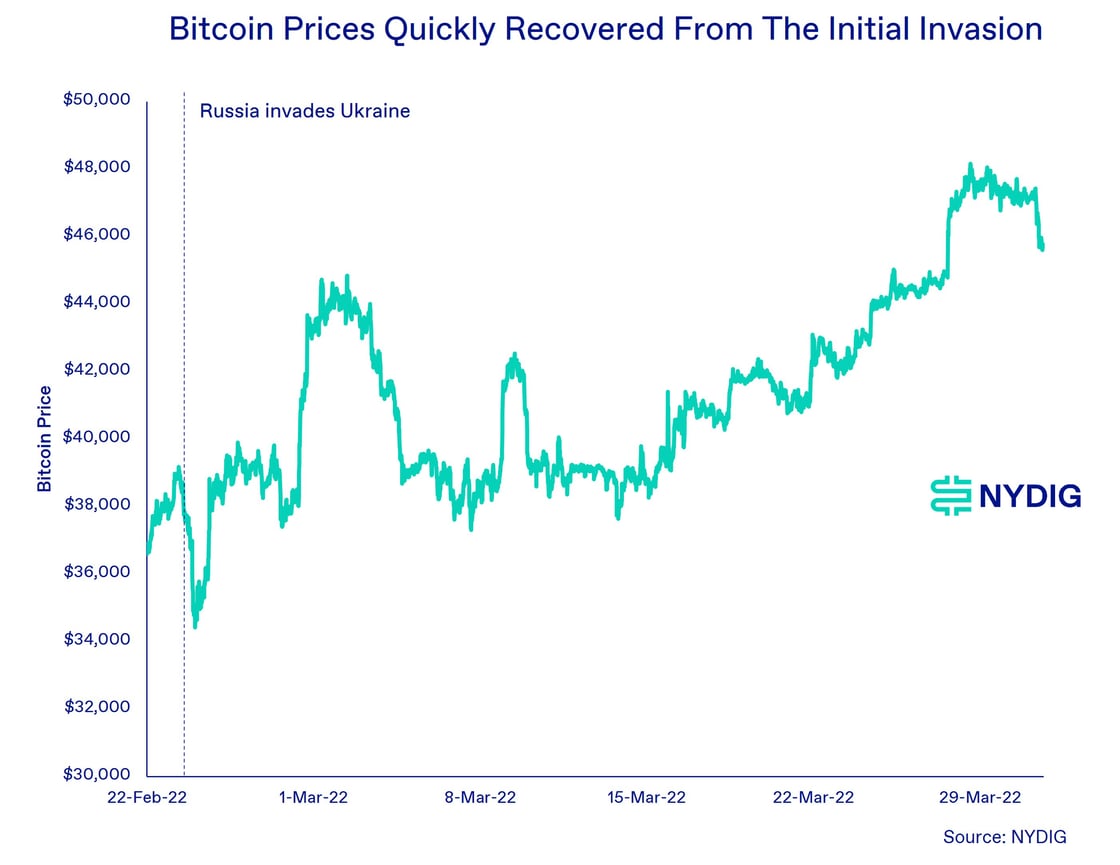

Ukraine Invasion Highlights Bitcoin's Benefits

On February 23, Russia invaded Ukraine. Bitcoin’s price initially reacted unfavorably to the news, dropping as much as 7%. But by the next day, bitcoin’s price had entirely recovered and then some. At quarter end, bitcoin sits at $45,596, well above the price before the conflict when bitcoin traded around $36,900.

What have we learned from this episode so far? First, price reactions based on first takes are not always the right ones. We have noticed this dynamic increasingly around FOMC rate announcements and CPI prints as well. Second, US officials are not worried about Bitcoin being used as a means of sanctions evasion. This has been echoed numerous times by various members of the current administration. Third, the value of a decentralized monetary system is on display during times such as these. Case in point is the tens of millions of dollars raised in short order from around the world to aid Ukraine in its national defense. Thanks to the speed of settlement and low transaction costs, Ukraine has been able to rapidly collect the funds and use the proceeds to purchase military supplies such as bulletproof vests. Bitcoin can also be used as a store of value in times like this. In fact, its price appreciated while the Russian ruble faltered. Finally, because bitcoin can be easily “carried” across borders by memorizing a 12-24 seed phrase, it served as the ultimate wealth preservation tool for those uprooted by the war.

Public Crypto Companies Lag Bitcoin

Although bitcoin managed to end the quarter close to flat, the same cannot be said about crypto-related equities. Miners returned -22.7% in the quarter, while non-miner digital asset companies returned -22.1% (both figures weighted by market cap). These companies, on average, not only underperformed bitcoin but also equities more broadly; the S&P 500 was down -4.6% and the Nasdaq Composite fell by -8.9%.

The revenue of non-miner digital asset companies, whose business tends to be driven by (especially retail) crypto transaction volume, is driven by two factors – price and volatility. Increasing prices and higher volatility both tend to drive more attention to the asset class and thus lead to more trading. And most digital asset companies, especially exchanges, do not generate all of their revenue from bitcoin. In fact, in 2021, Coinbase only generated a quarter of its transaction revenue from bitcoin. So, looking across the entire crypto universe, this quarter was tough for these companies on both fronts. Although bitcoin was able to finish the quarter unscathed, most digital assets, including ETH, were down on the quarter. And most cryptocurrencies were less volatile in 2022 than they were in 2021. The result was less trader interest, lower trading revenue, and thus less love from the investment community for these companies’ stocks.

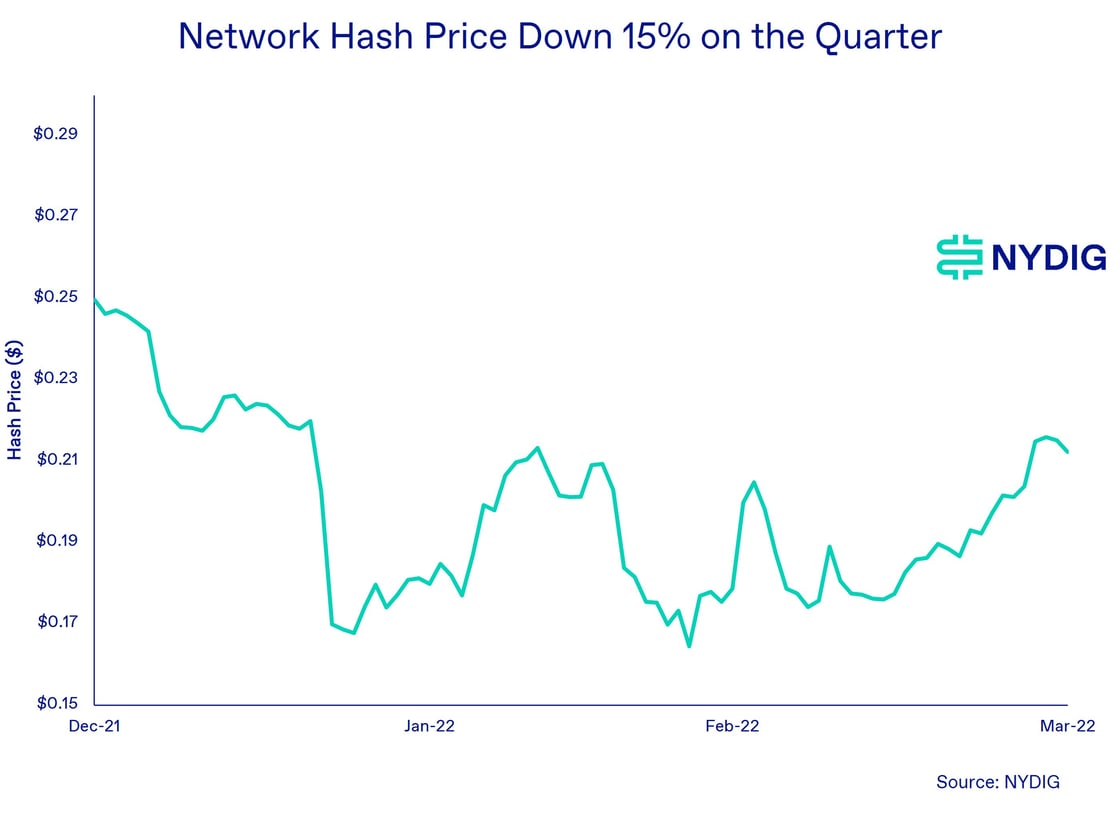

Miners, on the other hand, are only exposed to bitcoin prices and the network hash rate, which can be combined into a metric called “hash price.” Hash price measures the revenue, in dollars, generated by a unit of hash rate. Bitcoin price affects this measure because when bitcoin prices are higher a mined bitcoin is more valuable. The network hash rate fits in because when the network hash rate is higher, it is harder to generate bitcoins, and thus revenue decreases. Because the network hash rate has increased as bitcoin’s price remained close to flat, the hash price has fallen 15% in the quarter. Meanwhile, many public miners have seen difficulty in sourcing new equipment and bringing it online, leaving them behind.

Crypto-related equities can be attractive investments in their own right, but these examples go to show why they cannot be viewed as bitcoin replacements in a portfolio. The tracking error of these equities to bitcoin is generally above 100% – this tracking error is driven by the unique characteristics of each of these companies. And even beyond industry-specific idiosyncrasies, companies can also have their own managerial and operational risks. This means that a bitcoin rally does not guarantee a profit in a crypto equity investment.

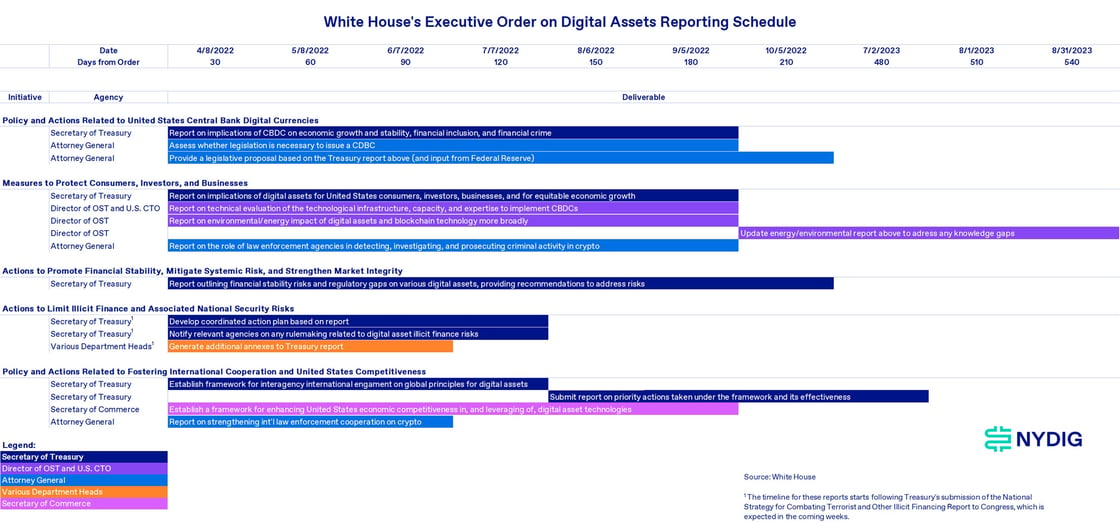

Since its existence became known in a Bloomberg article at the end of January, the White House’s Executive Order on digital assets had been a source of much consternation for crypto investors. On March 9, however, the White House finally laid out the order on “Ensuring the Responsible Development of Digital Assets.” We viewed this order as more of an even-handed fact-finding effort, rather than anything onerous or heavy-handed. Over the coming months, the White House is tasking several regulators and agencies with a fact-finding mission. This will likely result in consultations, conversations, and perhaps many months down the road, legislation. The government does not work fast, which is good in this case. Given the tone of the Executive Order, we would expect the outcomes to be supportive of innovation while at the same time protecting national security interests. We think increasing regulatory clarity is something that will be welcomed by investors in the space.

Since the start of the rally in the price of bitcoin, which is over 2 years old now, two trends have been persistent: bitcoin being purchased on exchanges and withdrawn for long-term holding, and more bitcoins being held for longer. The combination of the two paints the picture of a limited supply asset being increasingly locked away.

Bitcoin as a Stablecoin Reserve

On February 22, the Luna Foundation Guard (LFG), a non-profit organized to support the Terra ecosystem (ticker LUNA), announced it had raised $1B to purchase bitcoin. This money would create a “foreign exchange” reserve for the TerraUSD (UST) stablecoin. Terra, a rapidly growing platform for the creation of algorithmic stablecoins, has seen significant growth as of late, especially in demand for its premiere stablecoin, UST.

Why would the LFG want to add bitcoin as a reserve? Simply, to reduce the risk to LUNA in the event of a downturn in demand for UST (link to our more in-depth analysis). At present, a decline in demand for UST can cause an increase in the supply of LUNA. The burning of UST causes an equivalent dollar amount of LUNA to be minted. This could negatively affect the price of LUNA. If perpetuated, LUNA might end up in a tailspin, something the LFG is trying to head off. A bitcoin reserve would allow the LFG to send UST burners bitcoin in addition to creating new LUNA supply, buffering the impact to LUNA. Investors may also use bitcoin in addition to LUNA to mint UST, adding to UST’s bitcoin reserves. In our view, inserting bitcoin into the LUNA-UST mechanism reduces both ends of the return distribution for LUNA — and makes UST look a bit more like a traditional stablecoin.

LOOKING AHEAD TO 2Q22

As mentioned above, the second quarter of the year has historically been more positive for bitcoin prices than the first. We hope that this provides a positive lift for bitcoin prices. In light of that backdrop, there are several other items to look forward to in the coming few months.

Conference Circuit Heats Up

The second quarter typically features a high volume of crypto-related conferences, which serve as the backdrop for product announcements, new business initiatives, and technology development unveilings. While it is impossible to predict what will be announced this year, we think keeping an eye on the calendar will serve investors well. The following is a list of some of the larger upcoming conferences:

Bitcoin 2022: April 6- 9

Crypto Bahamas: April 26-29

MIT Bitcoin Expo: May 7-8

Consensus: June 9-12

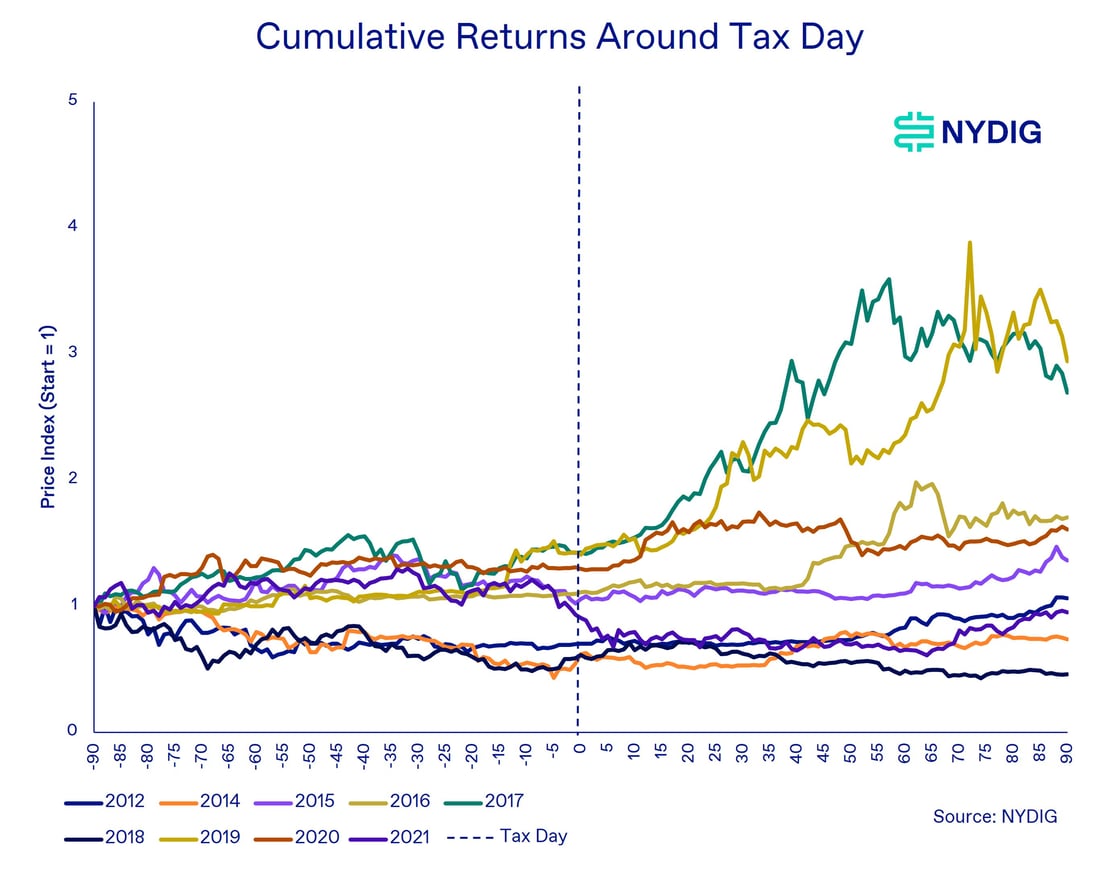

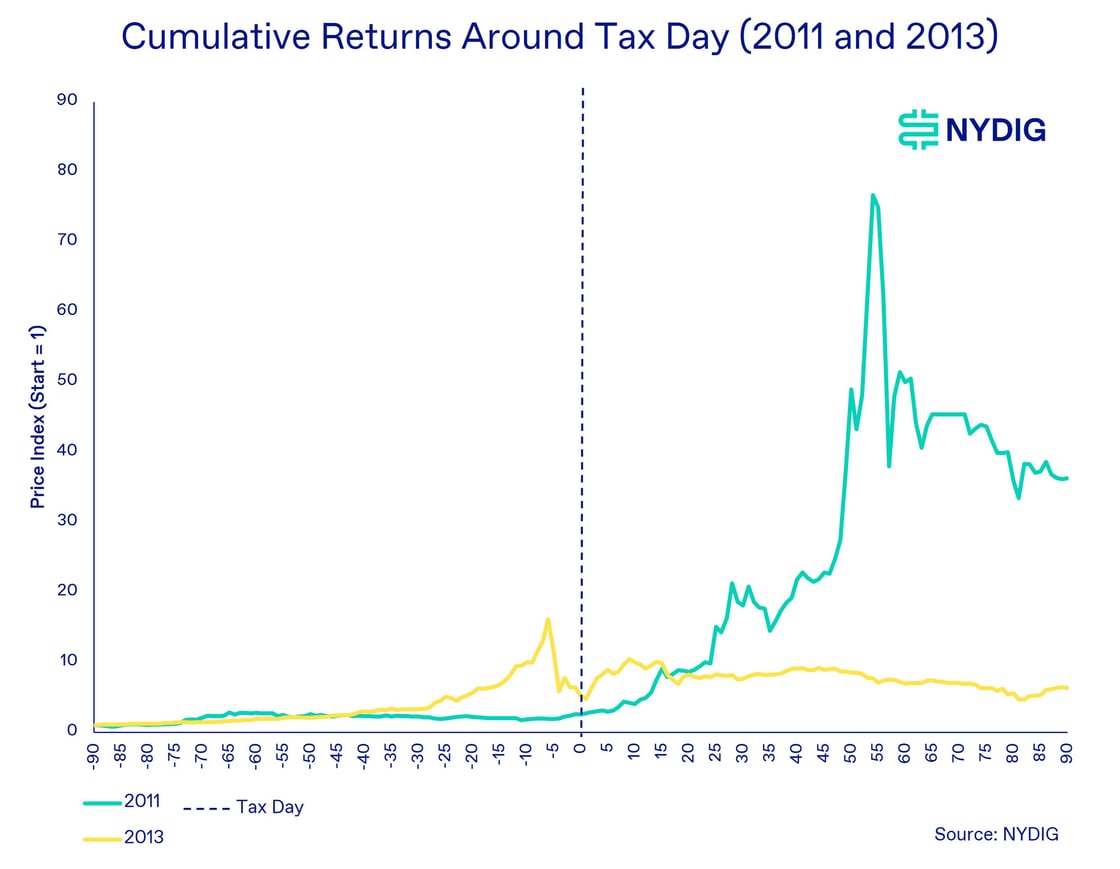

Tax Season, Potentially

One of the long-standing beliefs in the crypto community is that prices underperform ahead of the US tax filing deadline and then outperform after. The theory is that investors sell crypto to pay taxes owed on gains ahead of the filing deadline (April 18 this year) and then use proceeds from refunds after the deadline to buy more crypto. Unfortunately, the data on this phenomenon is mixed. While there have certainly been years of underperformance ahead of tax day and outperformance after, the trend is not consistent. The following charts highlight this trend, with the years 2011 and 2013 separated into their own graph because of their disproportionately high returns.

Markets Giving Fed Leeway to Raise Rates

The market is already implying a much more hawkish stance by the Federal Reserve than anticipated at the end of last year. On January 1, 2022, the market was prepared for about three 25bp rate hikes. Now, that number is closer to nine. This seemed to have deleterious effects across risk assets, with bitcoin and equities both selling off. The good news, though, is that this hawkishness now appears priced in. While the Fed can certainly hike more — which would likely provide more downward price pressure, based on bitcoin’s recent price reactions — the markets are already placing an impressive bogey on it. How the Fed deviates from expectations on that front remains to be seen.

The other Fed action to look out for is how it treats its balance sheet. We will likely hear how the Fed plans to manage its balance sheet at the May 4th meeting. Like with rate hikes, it appears likely that the more hawkish the posture, the worse the effect on bitcoin prices, so we will be closely watching for any indication of how the Fed may proceed.

Thanks for joining us again this week. Please reach out with any questions or comments.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication, the recipient acknowledges its understanding and acceptance of the foregoing terms.