Backers of the Terra platform (LUNA) are buying bitcoin to create a strategic foreign exchange reserve to bolster the UST stablecoin.

This bitcoin reserve is intended to support LUNA, the native token of Terra, in times of high redemptions for UST.

Interest in UST has been high, in part because the DeFi Anchor Protocol has been paying 19.5% annualized interest rates to UST holders.

$3B looks like the short-term ceiling for bitcoin purchases. The $10B number widely circulated on social media appears to be a longer-term aspirational target, rather than an imminent checkpoint.

While it is difficult to judge the short-term price impact, over the intermediate term, buying $125M per day should lend support to bitcoin’s price.

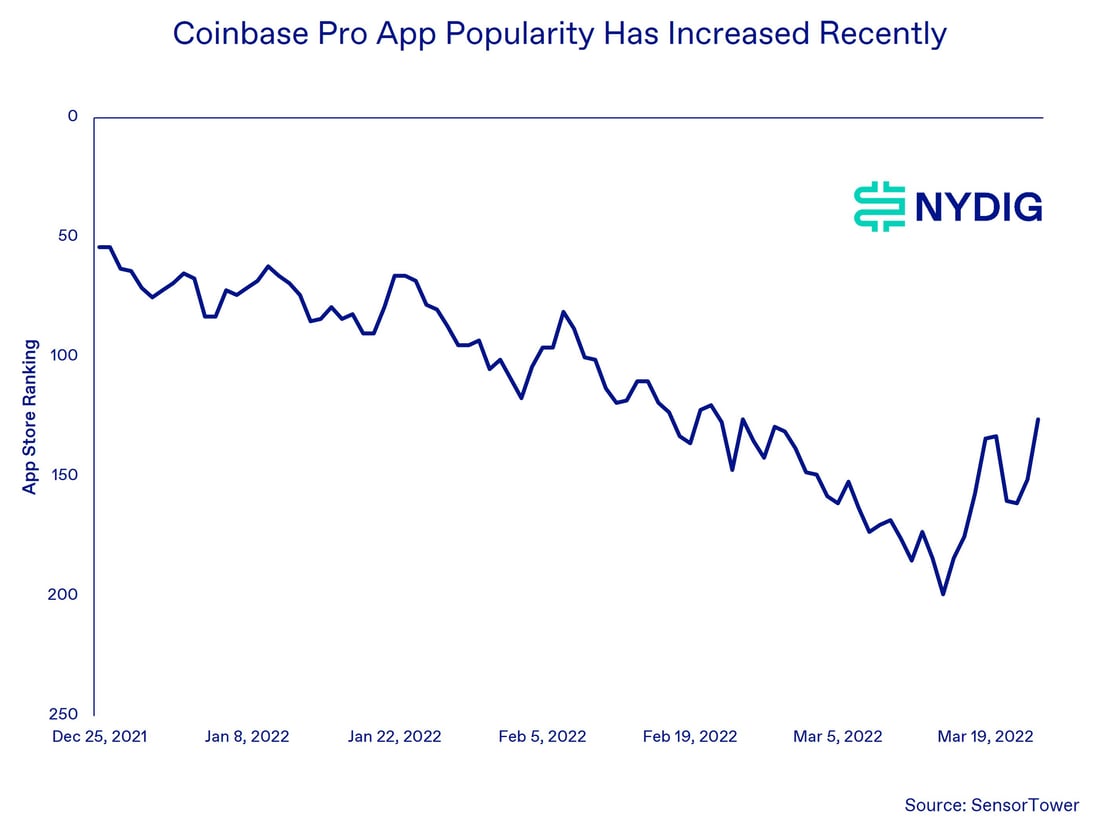

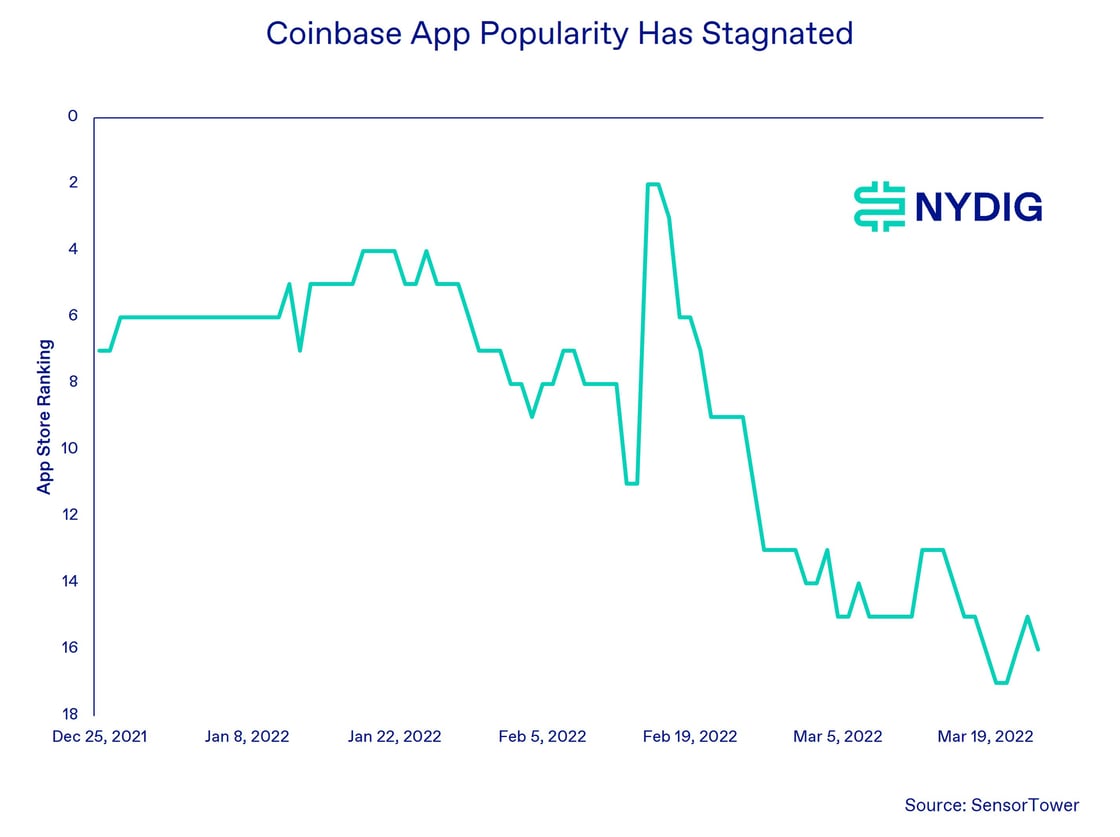

App rankings show that more sophisticated crypto investors appear to be returning to the markets, while traditional retail appears to be quiet.

Bitcoin Becomes a Stablecoin Reserve for Terra

On February 22, the Luna Foundation Guard (LFG), a non-profit organized to support the Terra ecosystem (ticker LUNA), announced it had raised $1B to purchase bitcoin. This money would create a “foreign exchange” reserve for the TerraUSD (UST) stablecoin. Terra, a rapidly growing platform for the creation of algorithmic stablecoins, has seen significant growth as of late, especially in demand for its premiere stablecoin, UST. While investors might be familiar with the concept of stablecoins, digital assets designed to mimic the value of fiat currencies like the US dollar, UST differs from reserve-style stablecoins such as Tether (USDT) or USD Coin (USDC). Those stablecoins hold USD balances in bank accounts and then issue digital assets on a 1-for-1 basis. UST is created by the redemption of LUNA, the native asset of the Terra platform. Investors wishing to mint (create) UST purchase LUNA and then burn (destroy) an equivalent dollar amount of LUNA, permanently removing it from circulation. Investors wishing to redeem their UST do the reverse, creating LUNA in an equivalent dollar amount as their UST, which is burned in the process. As demand for UST increases, the supply of LUNA, which has a capped supply to begin with, declines. This potentially leads to higher LUNA prices. This process also works in reverse. For those that don’t want to go through the minting process, UST is also available directly for purchase on exchanges. UST keeps its peg to the dollar via a combination of the mint/burn process and market activity by arbitragers.

20% Yields Drive Interest in UST

Why would investors want UST? Mostly because a decentralized finance (DeFi) protocol on Terra called Anchor Protocol has been paying UST holders 19.5% annualized interest. Given where yields are across the credit and duration spectrum, it should come as no surprise that 19.5% on a US dollar proxy is highly enticing. So while in theory the supply of credit should be offset by demand, there is a significant mismatch, with $11.4B in deposited UST and $2.8B in borrow (data here) — and this is even with borrowers paying net about 3% per annum. Where is the remaining yield paid from? The answer is from Anchor’s reserve balance, which currently has about $390M UST. This reserve balance collects fees from borrowers, but the money going into the pockets of depositors has far outweighed these fees. Because of this imbalance, the reserve had to get topped off in February with $450M of fresh UST after it nearly ran out. As a more permanent solution to the problem, yesterday the community voted to create a semi-dynamic deposit rate to match the market demand more accurately from borrowers, implying that yields for depositors should fall significantly. One important caveat – even with the community vote to reduce rates, this may look like an unsustainable liquidity bootstrapping mechanism. However, the LFG has support from LUNA's creator, Terraform Labs (TFL), which presently owns nearly $34B of LUNA and UST and other assets, meaning substantial support could be provided if need be.

Bitcoin as a “Forex Reserve”

Why would the LFG want to add bitcoin as a reserve? Simply, to reduce the risk to LUNA in the event of a downturn in demand for UST. At present, a decline in demand for UST can cause an increase in the supply of LUNA. As mentioned above, the burning of UST causes an equivalent dollar amount of LUNA to be minted. This could negatively affect the price of LUNA. If perpetuated, LUNA might end up in a tailspin, something the LFG is trying to head off. A bitcoin reserve would allow the LFG to send UST burners bitcoin in addition to creating new LUNA supply, buffering the impact to LUNA. Investors may also use bitcoin in addition to LUNA to mint UST, adding to UST’s bitcoin reserves. In our view, inserting bitcoin into the LUNA-UST mechanism reduces both ends of the return distribution for LUNA — and makes UST look a bit more like a traditional stablecoin.

$3B Seems like the Short-Term Ceiling in Purchases, not $10B

The technological infrastructure to support this semi-reserve policy is not yet fully ready, nor does it presently have $10B as was acknowledged by Do Kwon, the CEO of TFL and founder of Terra. This has not stopped the LFG from beginning to purchase bitcoins for the reserve. The long-term goal is to hold $10B, but the more realistic short-term goal is closer to $3B. It is unclear exactly how many bitcoins the LFG has already purchased. In terms of funds available to buy more BTC, right now we know that the LFG has raised $1B, plus has nearly $750M of LUNA ($400M here and about $350M sent here, plus likely another nearly $1.3B of other non-USDT stablecoins (these coins could have some overlap with the $1B raise). Absent additional fundraises or contributions from TFL, $10B is a long way away. While the total value of the proposed bitcoin purchase has garnered attention, what is more important is that this signals that corporates, diversified investors, and even protocol developers see bitcoin as the premier digital asset.

How Would a $3B Purchase Affect Bitcoin’s Price?

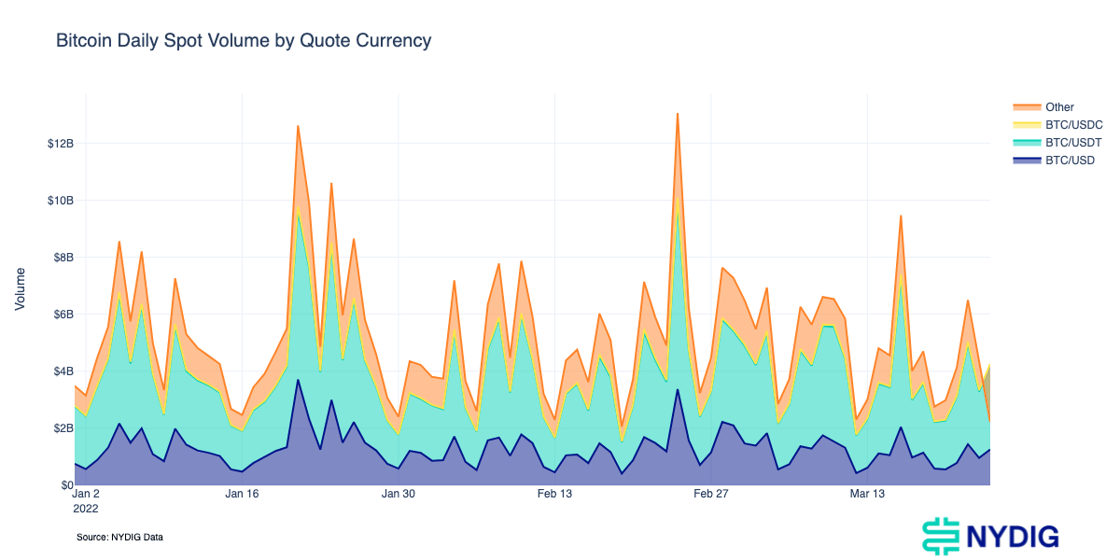

The LFG seems to be sending $125M clips of its Tether (USDT) reserve to exchanges to buy bitcoin. These transfers started on Tuesday and have occurred daily since then. If the LFG intends to purchase $3B of bitcoin at $125M/day, that is 24 days of buying. Across the exchanges we track, $125M is significant compared to the $5.2B in average daily volume of spot bitcoin trading. That’s especially true because the volume is fragmented across exchanges. How it impacts price in the short term will be subject to trade execution. At a minimum, it should be supportive of bitcoin’s price over the intermediate term.

More Sophisticated Crypto Investors Return to the Market While Traditional Retail Remains Quiet

Looking at the rankings for Coinbase Pro app downloads vs the regular Coinbase app leads us to believe more sophisticated investors are returning to crypto markets even as traditional retail remains quiet. Rankings for the Coinbase Pro app bottomed on March 15 and rebounded significantly, while rankings for the Coinbase app have seemed to be moving sideways. The Coinbase app did see a big jump in downloads after the Superbowl, which featured a prominent Coinbase ad, but that spike in interest appeared to be short-lived.

Market Update

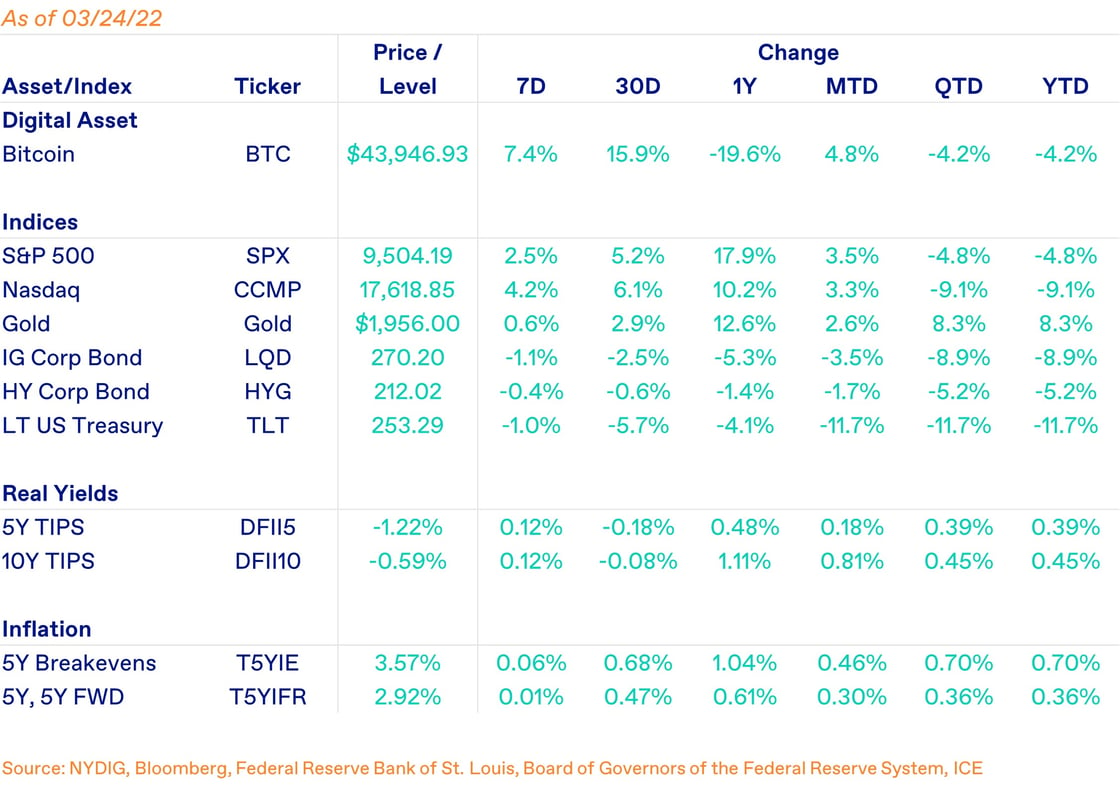

Bitcoin continued to rally this week, up 7.4%. The asset is now down only 4.2% year to date, outperforming stocks and bonds. The level to get back to flat on the year is $45,867.86. Stocks also had a strong week, with S&P 500 up 2.5% and Nasdaq Composite up 4.2%. Gold was up slightly as real yields and inflation expectations ticked up. Bonds had a rough week with investment grade corporate bonds down 1.1%, high yield corporate bonds down 0.4%, and long-term Treasuries down 1.0%.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication, the recipient acknowledges its understanding and acceptance of the foregoing terms.