It was a tough quarter and year for bitcoin's price performance as both were marred by the failures of players across the industry.

The macro backdrop was more favorable for asset prices this quarter with declining rate expectations and easing inflation.

The collapse of FTX and Alameda dominated headlines this quarter and negated any benefit that bitcoin might have seen from an easier macro backdrop.

Regulation is top of mind with the events of 4Q creating urgency for greater clarity but also taking time to digest and ensure appropriate safeguards.

While bitcoin struggled this year, crypto-related equities fared even worse, perhaps owed to their operating leverage to digital asset price.

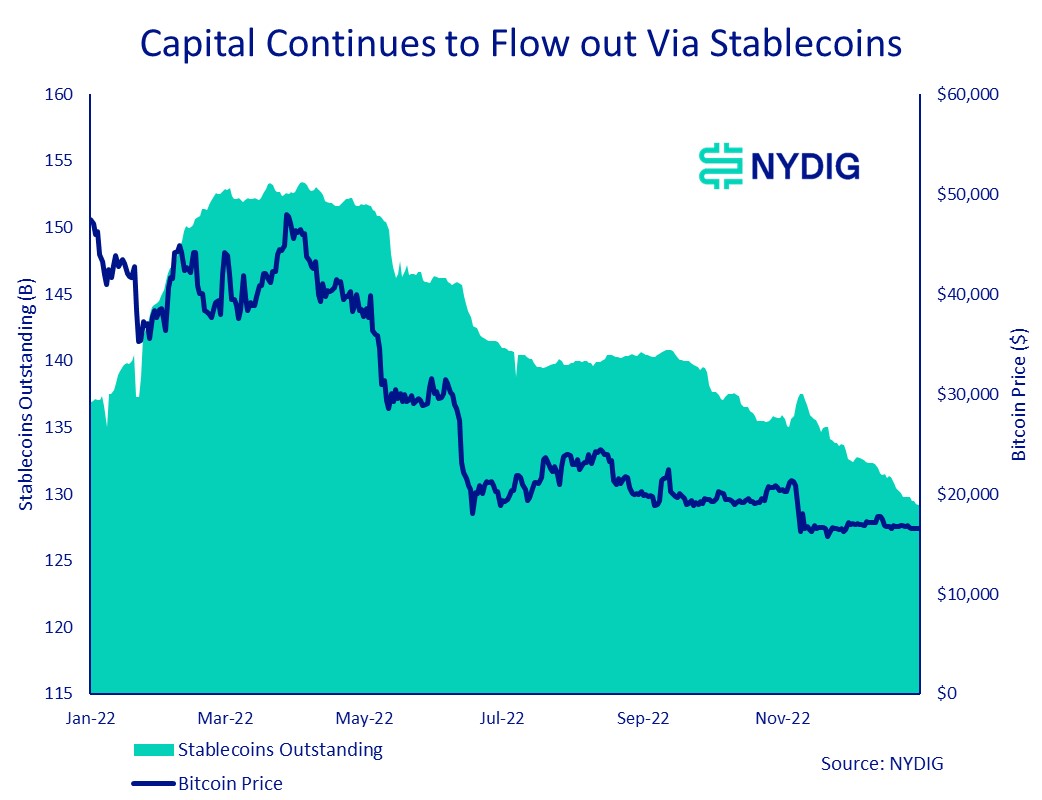

Flows into bitcoin funds were flat for the second straight quarter, but money continues to exit the crypto ecosystem by declining stablecoin supply.

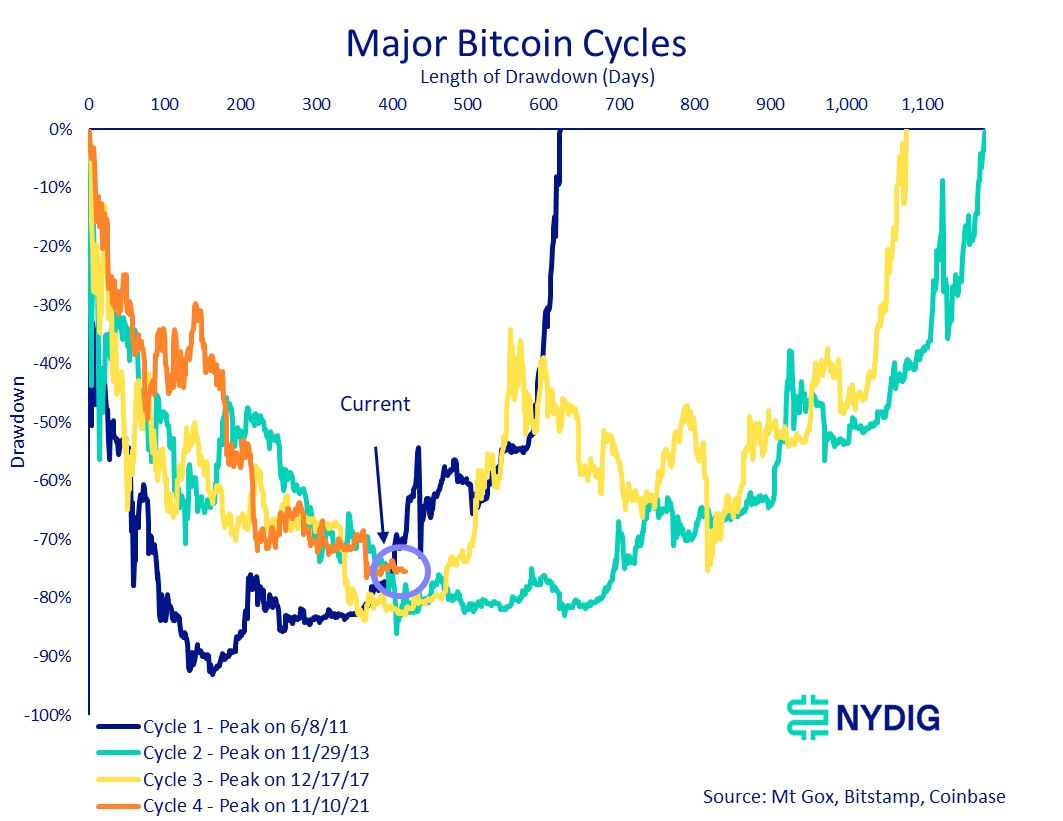

While the events that have transpired throughout the drawdown have been unlike any other cycle, the depth and duration look very similar to past cycles.

While past performance is no indication of future performance and in many ways we are in a new macro paradigm, investors should take solace in the fact that bitcoin has been in a similar situation several times in the past.

Bitcoin's next cycle catalyst had never been obvious at the cycle bottoms of 2015 and 2018, so we remain open-minded. The reality may be that these cyclical price waves may be indicative of investor over and under confidence about an axis of secular growth.

Performance Review

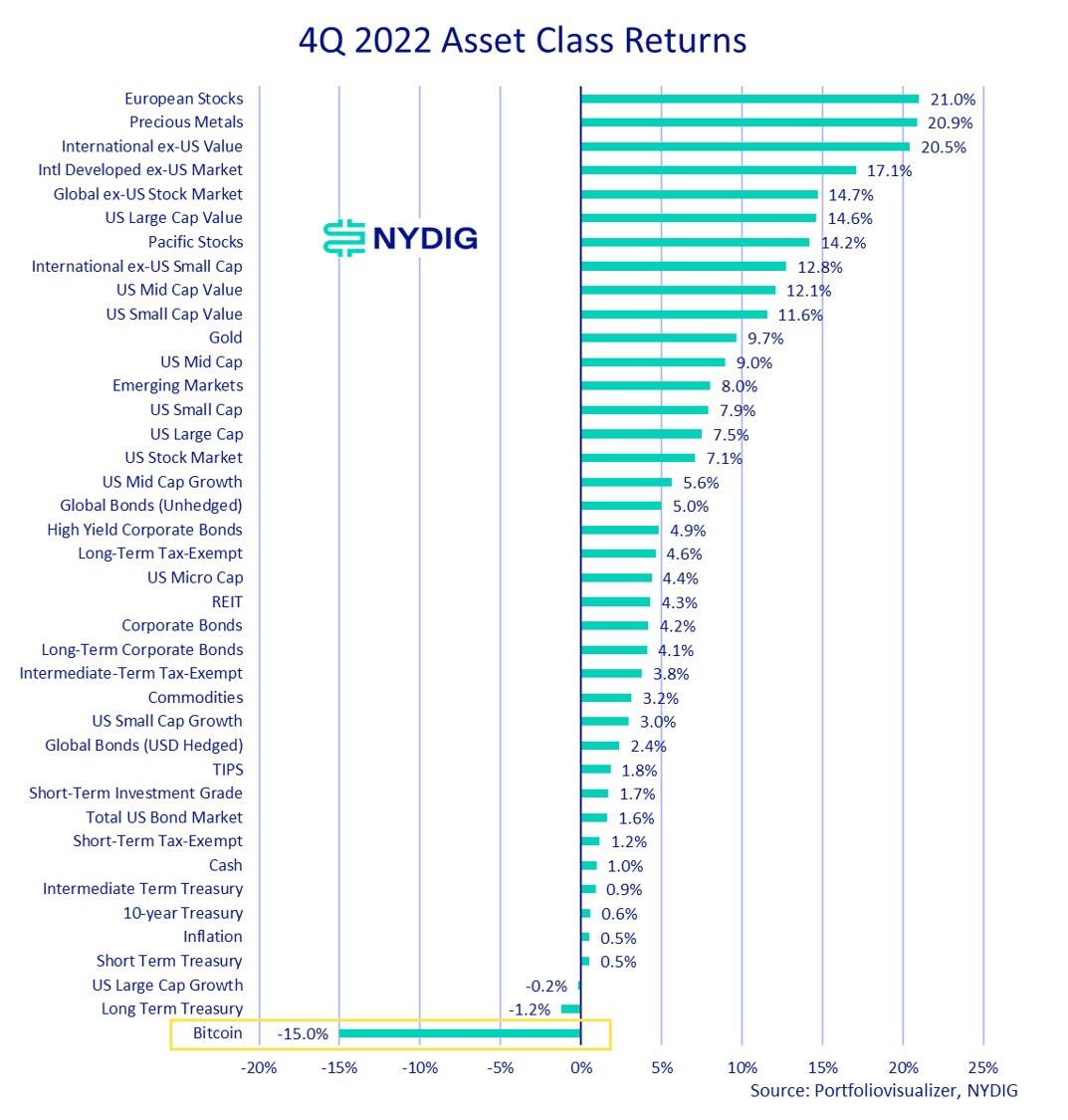

Bitcoin Posts Quarterly Decline Amidst a Tough Year

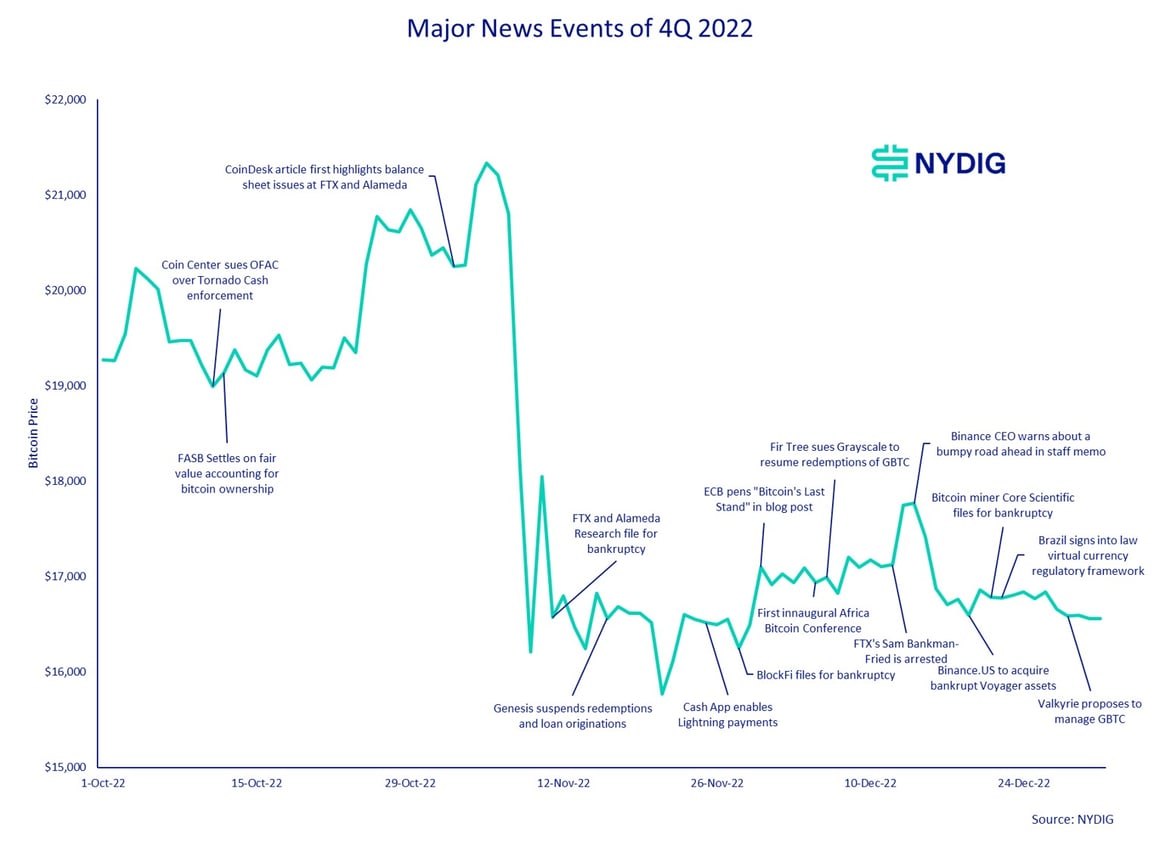

There’s no way to sugarcoat the fact that 2022 was a tough year for bitcoin’s price performance and 4Q was no exception. The price of bitcoin fell 15.0% during the quarter amidst market volatility induced by financial distress, and ultimately the bankruptcies of several centralized players in the crypto industry. Price performance was not an indictment of bitcoin per se, but rather it was of the faulty operations of some of the players in the industry, such as FTX, Alameda Research, and Genesis Global Capital, plus a variety of smaller players.

The frustrating thing about this quarter's price action was that it appeared that bitcoin had put a bottom in. Before the exposé of the inter dealings between FTX and Alameda by CoinDesk’s Ian Allision, which must be the scoop of the year, bitcoin had broken through the $20K barrier amidst a rally in other risk assets. Had it not been for the collapse of FTX and Alameda, price performance during the quarter might have been very different. But alas, it was not to be so. Bitcoin investors bear idiosyncratic (unique asset) risk as well as systematic (industry) risk, and this quarter's price action was a case of the latter rather than the former.

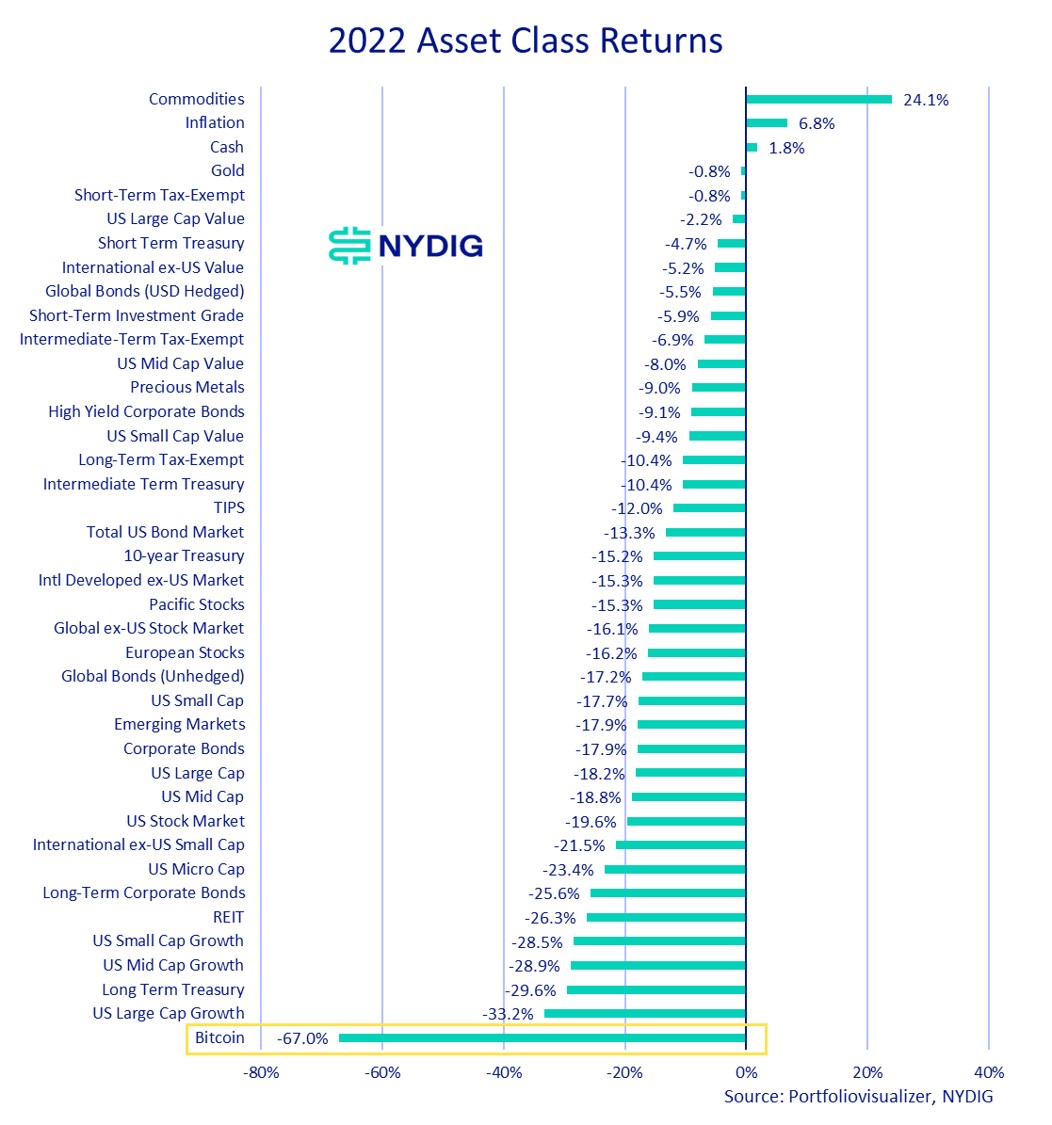

The full year 2022 was tough for nearly every asset class, with commodities and cash (3m T-Bills) being the only two asset classes up on the year. The Fed’s interest rate tightening campaign, which was telegraphed in November 2021 but began in actuality in March 2022 with the first rate increase, clearly had an impact across asset classes. This was felt by bitcoin, which was also affected by a host of crypto market dynamics this year, including the failures of centralized platforms and players as well DeFi applications and platforms, such as Terra (LUNA)/TerraUSD (UST).

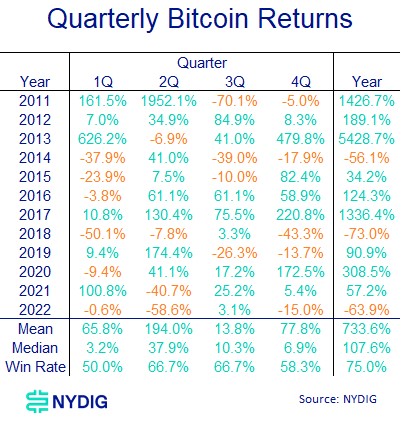

Yearly and Quarterly Returns Look Like Previous Tough Years

In many ways, bitcoin’s price performance this year has mirrored cycles of the past, albeit with different underlying factors. The end of the 2013 cycle was marked by China’s first clampdown on the asset while 2017 was a popping of the speculative Initial Coin Offering (ICO) bubble that largely took place on Ethereum. The odd thing about bitcoin’s price performance has been how regular the periodicity of these price cycles have been. Roughly every four years, centered on bitcoin’s block reward halving, bitcoin exhibits an asymptotic price rise which is followed by a steep drawdown in the years 2014 (-56.1%), 2018 (-73.0%), and 2022 (-63.9%). Important to note in the following table, 4Q has been typically one of bitcoin’s better quarters, except for years when bitcoin was down substantially. In those years, not even 4Q seasonality saves bitcoin.

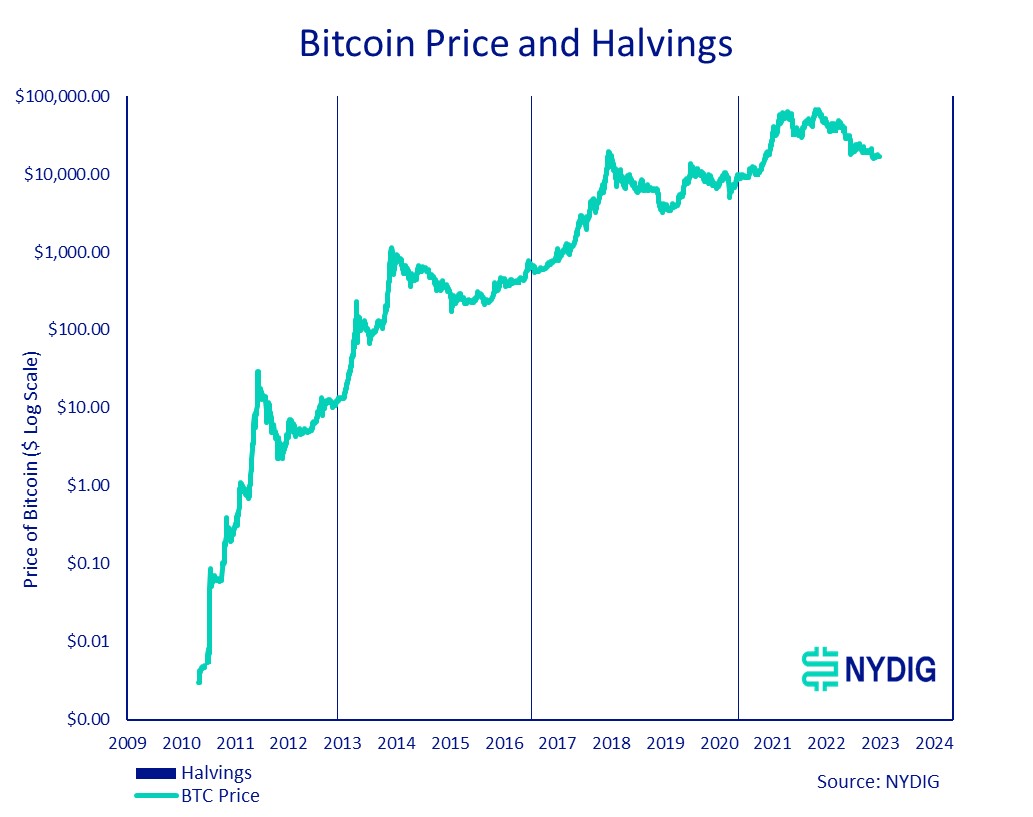

The repeating price pattern becomes a bit more obvious when graphed with the halving events, with the halvings themselves marking about halfway between cycle peaks.

Price Cycles – We Have Been Here Before

Using this cyclical price pattern, we have identified 4 price cycles that coincide with these halvings, and an inspection of the drawdowns yields some valuable insights. If there is one overarching takeaway we could impart on what has been a tough year, it is that we have been here before. While prices set a new cycle low in the fourth quarter, and there is no guarantee that was the lowest price we will see in this cycle, bitcoin has suffered from drawdowns of even greater magnitude and duration than the current one. If the recent low does prove to be the cycle low, it would be roughly in line with the duration of the previous 3 cycle drawdowns and the peak-to-trough decline would continue the pattern of increasingly more shallow drawdowns.

This all makes sense to us in the context of bitcoin’s repeating price patterns. However, bitcoin did violate a pattern of previous cycles. This drawdown bitcoin fell through the peak price of the previous cycle, in this case, $19,891.99, something it had never done before. It may be that bitcoin broadly adheres to some pricing patterns, like the 4-year patterns, but a prescriptive set of rules may be a bit too strict.

The collapse of centralized players and the ensuing financial contagion not only was the theme of the quarter, but also the year. The dramatic events of 4Q centered around the FTX crypto exchange and its closely related proprietary trading firm, Alameda Research. Their collapse had knock-on effects for other players in the industry, lender BlockFi filed for bankruptcy, Genesis Global Lending halted loan origination and redemptions (with perhaps implications for the broader Digital Currency Group (DCG) portfolio of companies), the exchange Gemini halted its Earn program, and a host of other funds connected to these entities suffered serious financial hardships.

The frustrating thing about the events of the past year is that aside from LUNA/UST it had little to do with the technology of digital assets themselves and more to do with the poor business tactics of centralized players. Bitcoin technology had nothing to do with the events of the past year. And for a technology created to remove trusted intermediaries from financial systems, it certainly was the actions of central financial actors that were responsible for the calamity this year. One thing for sure is that in the future the activities of other players in the industry need to be of paramount consideration.

Inflation Shows Signs of Abating

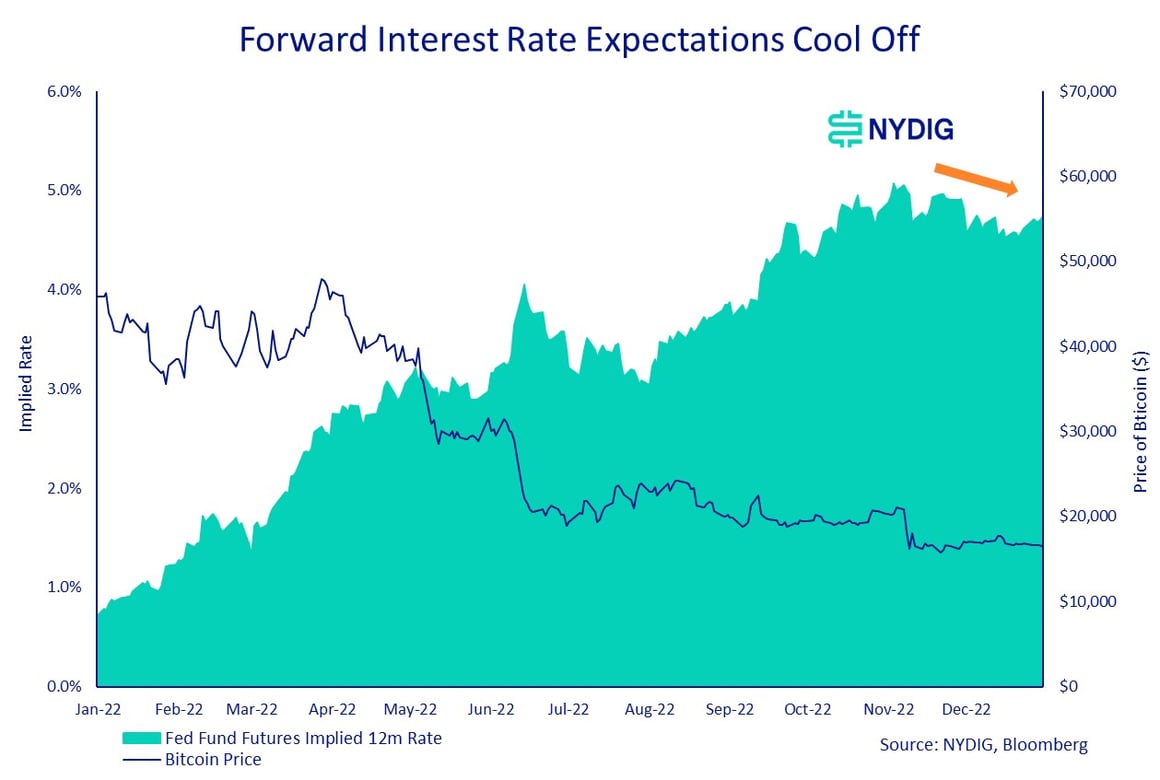

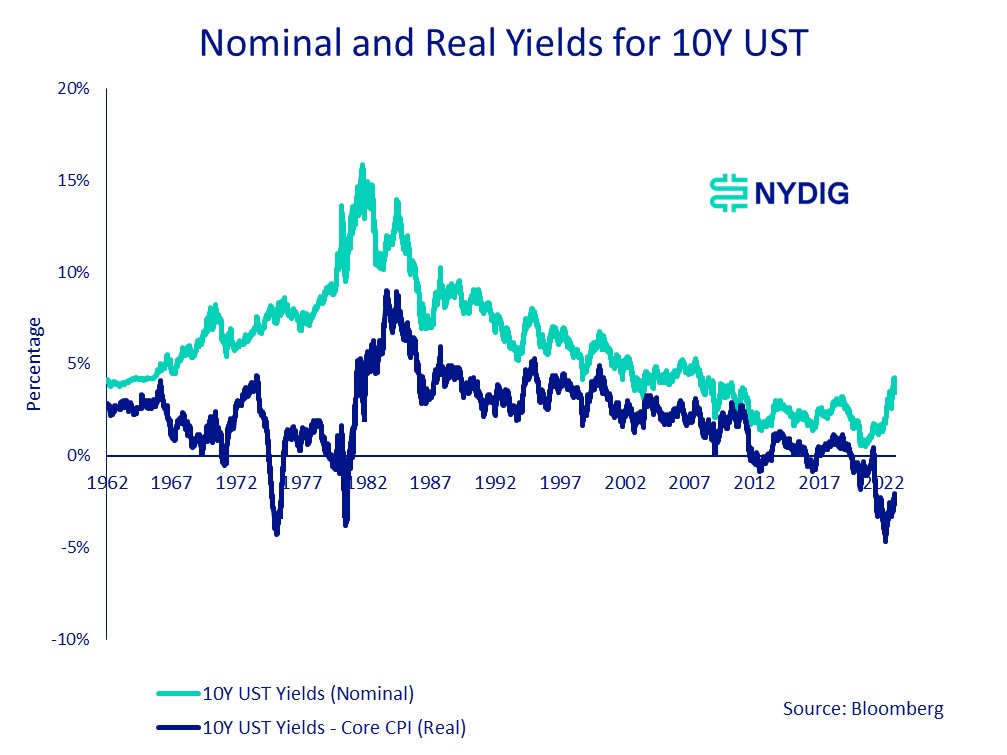

Since the Fed began to signal its desire to increase interest rates in November of 2021, risk assets, including bitcoin, have had a tough go of it. This quarter, however, inflation has shown some signs of abating, leading Fed officials to soften their stance on future rate increases. It was against this backdrop that risk assets like equities rallied and we guess that bitcoin would have as well had it not been for the events surrounding FTX. Certainly, the precipitous decline of most financial assets over the past year has affected household wealth and aggregate demand and with it prices. It remains to be seen if inflation is really under control, however. During the inflationary period of the 1970s and early 1980s, inflation remained stubbornly high, and it required a second rate hike campaign before it was effectively stamped out. We would not be surprised to see a similar dynamic here, where the Fed lets its foot off the rate accelerate only to find inflation to be stubbornly persistent.

Forward Rate Expectations Cool Off

For the past year plus, rising interest rates to combat inflation have been THE macro topic and one that has impinged on asset prices, including bitcoin. Investors got a reprieve during the quarter as 12-month forward rate expectations determined by Fed Funds futures declined. As we mentioned previously, that was a boon to other asset classes but the dramatic events that embroiled crypto markets overshadowed that.

Dollar Weakness Fails to Help Bitcoin

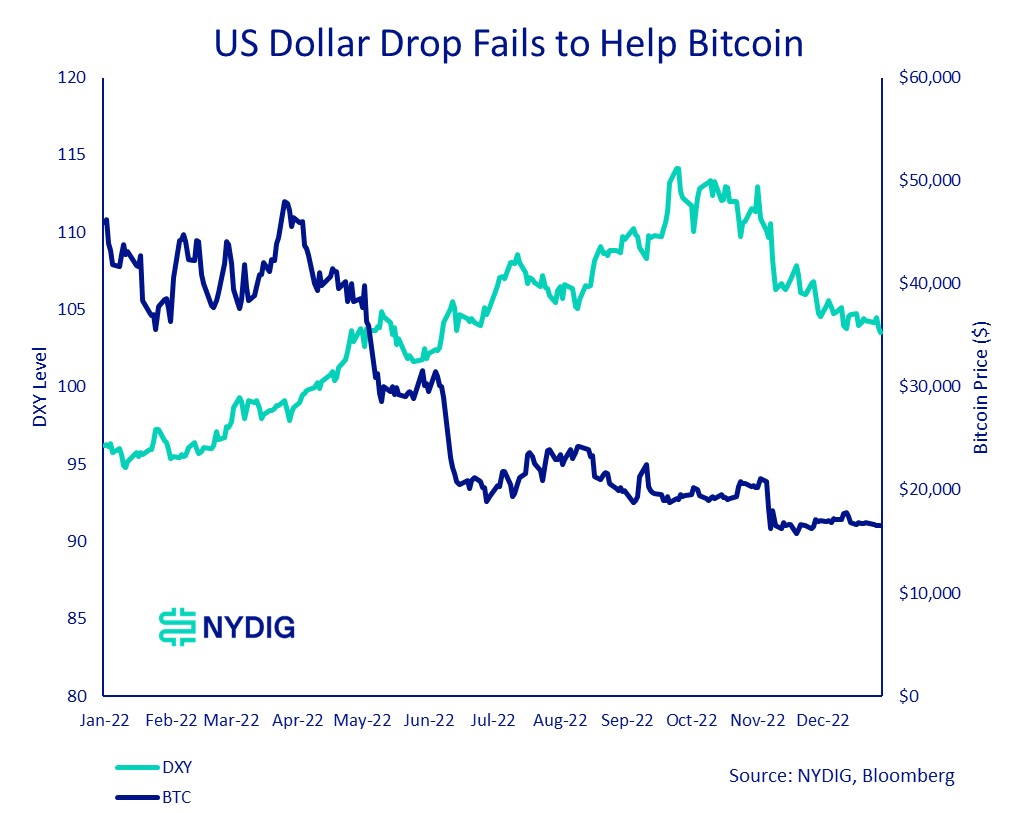

For the first half of 2022, there was a significant discussion about the US dollar’s strength and its negative impact on bitcoin’s price. We never bought it for the simple fact that the statistical relationship between the two, the R Squared of the year-over-year change in bitcoin price and the US Dollar Index (DXY), was never that strong (5.0%). However, this quarter the US dollar did weaken largely based on declining interest rate expectations, and clearly, bitcoin struggled. Not to discount this theory entirely, but it is important to understand that while the underlying drivers of the US dollar are complex, they most likely boil down to real rate differentials between the US and other sovereign nations and the US trade balance, its Current Account balance. Changes in real rates (10Y TIPS) have a much higher explanative power for non-income-producing assets like gold than the DXY (R Squared of 43.2% vs 10.2% since 2012). Changes in real rates are much less important for bitcoin than they are for gold, but conceptually we think that interest rates are one of the factors that affect the US dollar, which is why we focus on it instead of the US dollar.

Miners Continue to Feel the Pinch

The trend of falling hash price and miner inventory sales that were topical in 2Q and 3Q gave way to financial stress during the fourth quarter. Reorganizations, bankruptcies, and other workout situations have arisen amidst stiff headwinds for miners, which include high energy prices and production disruptions issues. The most notable piece of news was perhaps from Core Scientific, the largest public miner, who filed for bankruptcy protection on December 21. The network hash price is up off the lows but it’s easy to see miners are still not out of the woods yet. Even as miners continue to struggle, the Bitcoin network continues to operate as expected. Even the mining disruptions following the China ban in 2021, which saw the network hash rate decline by two-thirds produced little discernible impact on the network.

The Year of the Hack

It was a banner for crypto in one respect, but not one that we would like, hacks. Theft or loss of coins has always been an issue in crypto, but that used to be an issue relegated to centralized exchanges. With the advent of cross-chain bridges and DeFi, that risk has now migrated from centralized service providers, to on-chain code. DeFi applications such as sidechains and bridges, technologies not present on Bitcoin, were the source of billions of dollars of losses. Security firm SlowMist counted $3.8B worth of losses associated with hacks in 2022. Some noted hacks from the year were Ronin ($624M), BNB Bridge ($586M), Wormhole ($326M), Nomad ($190M), and Beanstalk ($181M). We are not against DeFi, but the technical community needs to build safer technology so these issues do not keep happening. This is even more pressing than just a crypto issue because state-sponsored entities like those associated with North Korea often pull off these hacks.

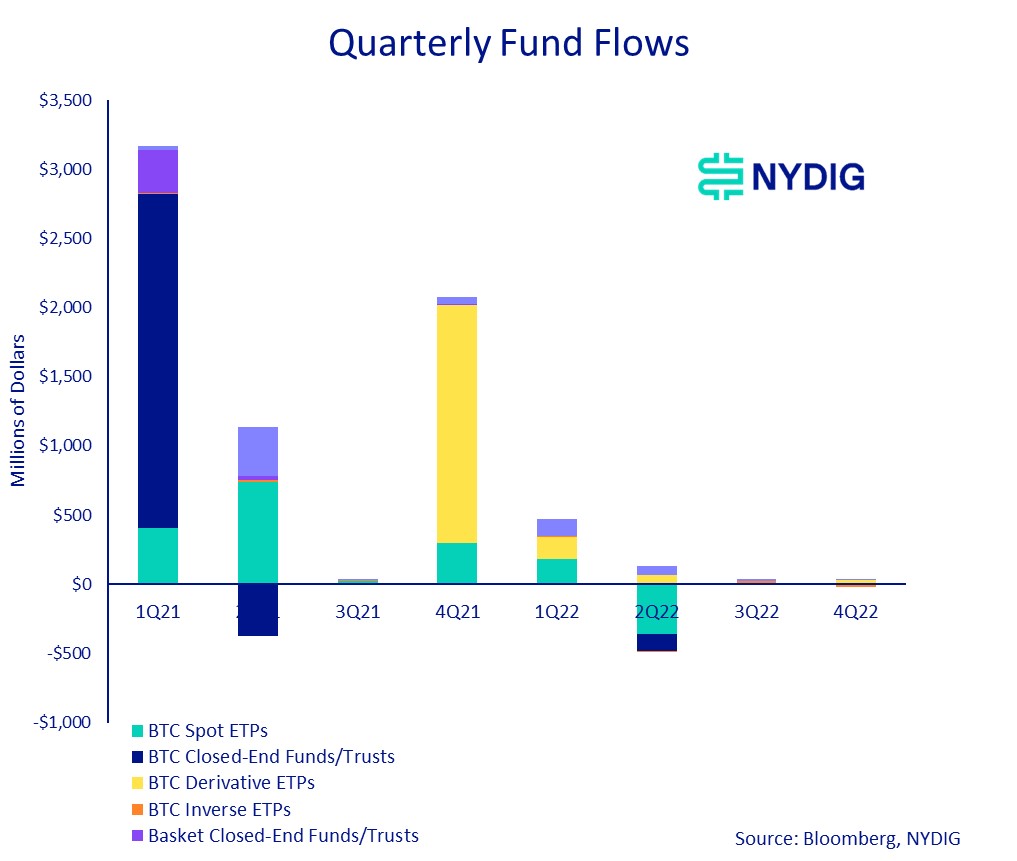

Funds Flow: Inflows Match Outflows for Second Consecutive Quarter

The flow of funds into funds listed on exchanges around the world or traded over the counter (OTC) essentially matched outflows, a similar dynamic that we saw last quarter. Net flows during 4Q amounted to -$4M while they amounted to +$6M during 3Q. This even balance between inflows and outflows dynamic was a significant improvement from 2Q, however, which saw net outflows of $352M. The full year did see positive inflows of $204M largely driven by 1Q. The last big influx of capital into the fund complex coincided with the launch of the ProShares Bitcoin Strategy ETF (BITO) in 4Q21.

Stablecoins Continue to Show Signs of Outflows

While flows into funds have been flat the past 2 quarters, money continues to flow out of the crypto ecosystem via stablecoins. While there have specific concerns about some of the issuers, such as the Binance Dollar (even though Paxos is the issuer), we think the broader trend is reflective of investors exiting the ecosystem in general. Typically if they were staying in the ecosystem but waiting to play a trade, they would park their funds in stablecoins, waiting for the right time. But this is different and the decline in stablecoins is more indicative of capital flight from the asset class. We will probably need to see these balances stabilize before the market can be considered to be on better footing.

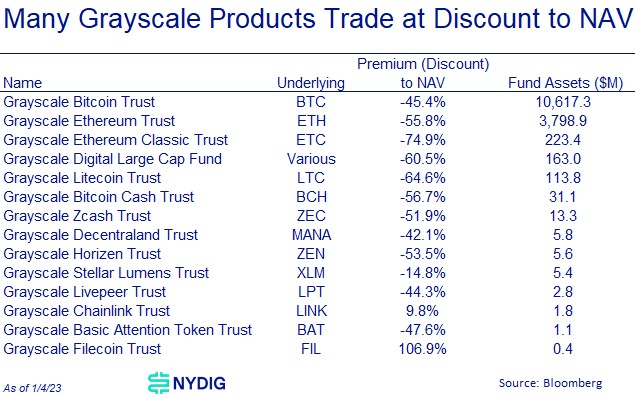

Grayscale Complex Under Scrutiny

The Grayscale fund complex, of which the +$10B Grayscale Bitcoin Trust (GBTC) is the crown jewel, has been under intense scrutiny throughout the year. This is in part because of the widening discount these products trade relative to net asset value (NAV) as well as business practices between Grayscale’s parent, Digital Currency Group (DCG), and DCG’s other subsidiary, Genesis Trading, whose lending business halted withdrawals during the quarter. During the quarter, hedge fund Fir Tree sued Grayscale and fund competitor Valkyrie Funds wrote an open letter suggesting that it take over as the trust’s sponsor. We have written about this discount to NAV dynamic numerous times, so there is little need to belabor the point, but we find it important to point out that this discount to NAV dynamic is not limited to GBTC nor the Grayscale complex. Most of Grayscale’s other products trade at a steep discount to NAV, plus other similar products managed by other sponsors exhibit a similar dynamic, so this is not just a Grayscale thing. For example, the Bitwise 10 Crypto Index Fund ($317M in AUM) currently trades at a 61% discount to NAV.

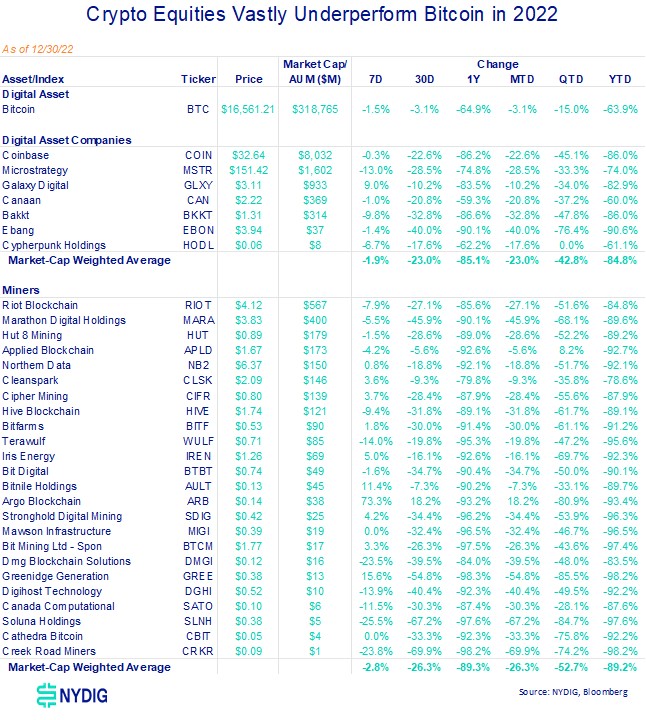

Crypto Equities Fare Far Worse than Bitcoin

If we think bitcoin struggled this year from a returns perspective, the equity of digital asset-related companies fared even worse. Through 12/30/22, the last trading day of 2022 (bitcoin had one more trading day than traditional markets), bitcoin was down 63.9% while digital asset companies were down 84.8% and miners were down 89.2% on a market cap-weighted basis. In some sense, this makes sense as these businesses have operating leverage to the price of digital assets, especially miners. Unfortunately, business operating leverage cut the wrong way in 2022 leading to much of their underperformance.

Regulatory Outlook Muddied by FTX Fallout

We had hoped that the end of 2022 would bring some regulatory clarity in the US. The Digital Commodities Consumer Protection Act (DCCPA) had been introduced in August, and the first version of the stablecoin bill from the House Financial Services Committee, both of which were highly watched items. Unfortunately, the events that unfolded in the quarter, the collapse of FTX and its related entities, resulted in legislative hearings rather than forward movement on legislation, but it is still unclear how the events that unfolded in 2022 will ultimately affect legislation. On one hand, it makes an argument for the expediency of regulation, but on the other hand, it requires a full unpacking of the events that recently transpired and likely adjustments to prevent them from happening again.

Looking Ahead to 2023

Macro Forces Still at Play

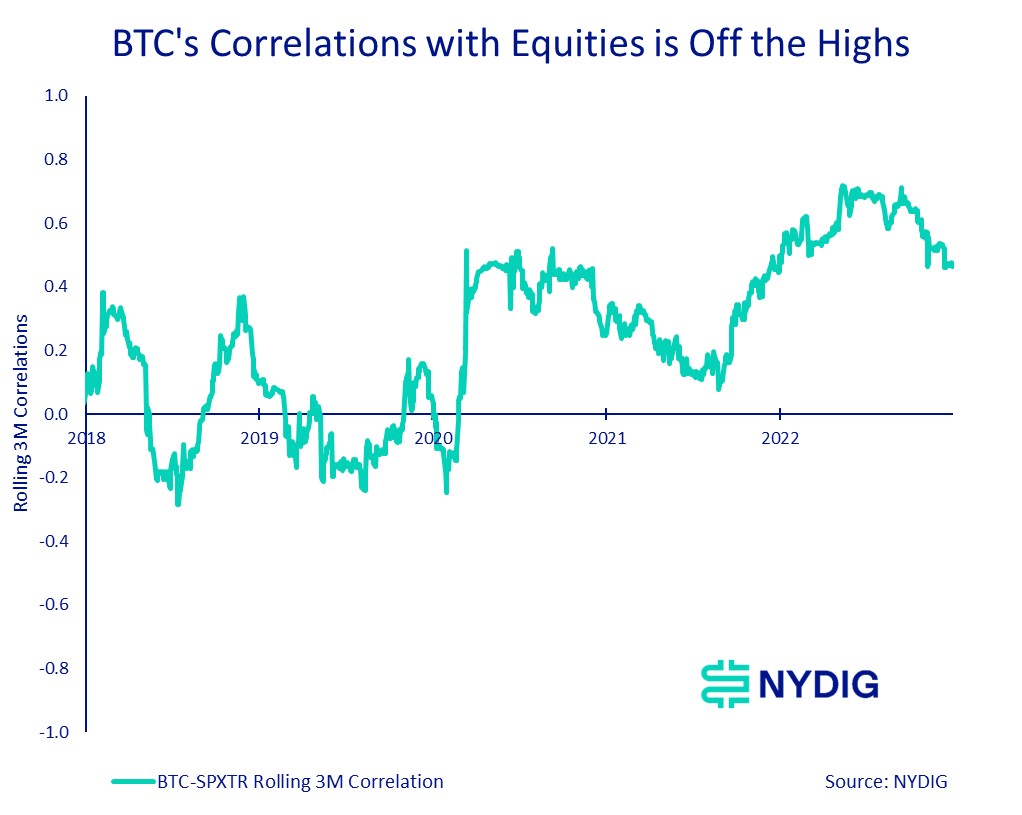

Macroeconomic factors have been a dominant force in financial markets, including crypto, since the onset of Covid-19. While we expect that to lessen over time, as bitcoin is still largely governed by unique factors, it is still important for investors to be mindful of the backdrop. Bitcoin’s rolling correlations with other asset classes, such as equities, have come off their summertime peak, but they remain elevated, especially compared to the pre-Covid era.

We have written about the interest rate and inflation environment, but the current inflationary environment and increase interest rate make for a unique backdrop, one that most professional investors have never experienced. For the past 40 years, declining interest rates benefitted from a “buy the dip” mentality supported by secularly declining interest rates, which is likely now over.

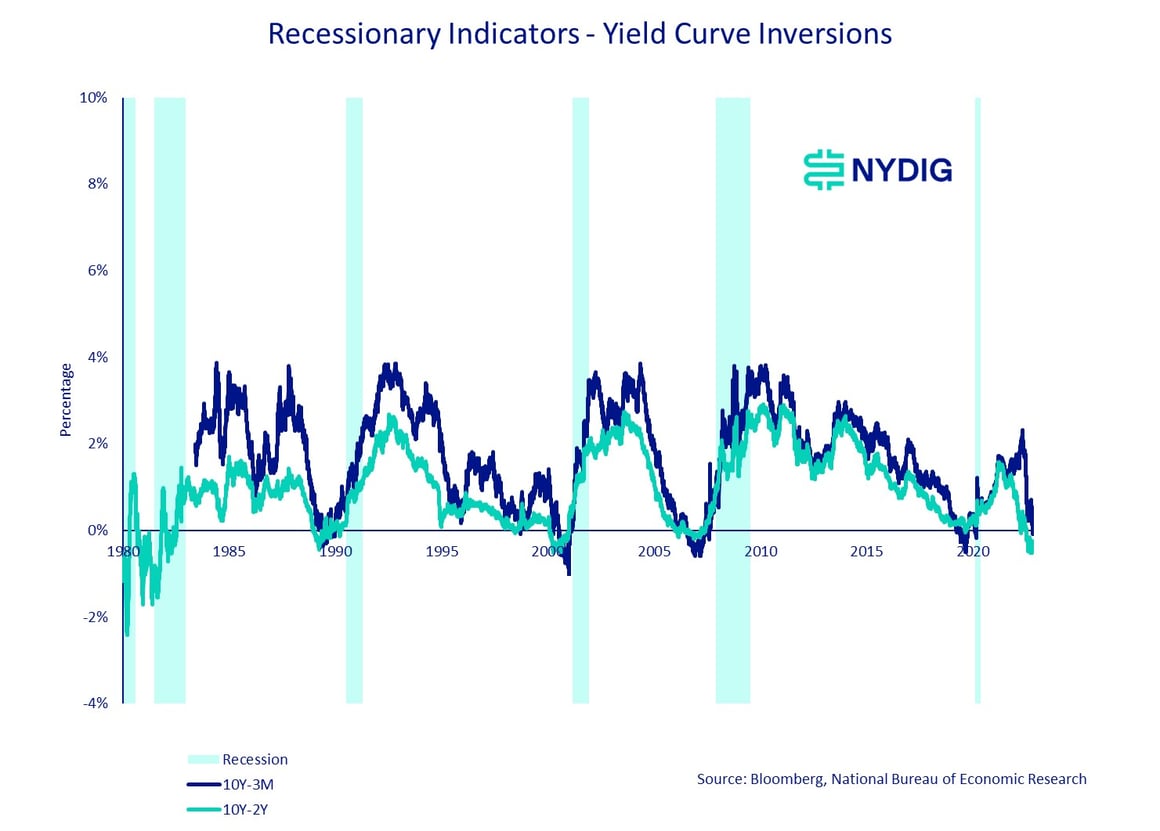

Complicating matters is the prospect of a recession in the US if yield curves are of any indication. Both the 10Y-2Y and 10Y-3M curves are inverted, strong predictors of recessions. Just how long it might take for a recession is still up for debate and even when it does occur (there will be a recession eventually, that we are certain of), markets are already well off their highs meaning the prospect of a recession might be less impactful to equity prices or bitcoin than it might have been in scenarios in the past. Bitcoin has only operated through the short but sharp recession induced by Covid-19 so it remains to be seen how it may fare in a different scenario, like a prolonged but more shallow recession.

Regulation Still Top of Mind, Timing on Clarity Uncertain

Regulatory clarity is still top of mind for institutional investors in this asset class. It is important to remind readers that in the US, bitcoin has a well-understood regulatory designation as a commodity, but the same cannot be said for the thousands of other coins out there. We are still hopeful for some movement on the stablecoin legislation and are eager to see the initial text of the act. The Digital Commodities Consumer Protection Act (DCCPA) from the Senate Ag Committee, which we had been hoping would be a 2023 event, may still be but its fate is less clear now given other events noted above. Investors continue to clamor for better regulation to prevent the events of 2022 from happening again, but how legislators and regulators intend to do that is not entirely clear yet. Regulation is coming, that we are certain of, and is likely to be supportive of bitcoin, but the same cannot be said for much of the rest of the industry. Once the rules of the road are better understood, institutional investors can more confidently deploy capital in the industry.

Technology Keeps Chugging Along

The technical development of Bitcoin has always been more evolutionary rather than revolutionary, unlike some other blockchains. Bitcoin has always focused on being the most secure decentralized payment protocol, forgoing novelty for safety. But that does not mean that Bitcoin as a technology or ecosystem doesn’t improve. Two new versions of Bitcoin Core were released in 2022, v23.0 and v24.0, each with new features and improvements. In addition, there were new releases of Lightning software LND, Core Lightning, and Éclair.

The Lightning Network continues to grow in network capacity as measured by the number of bitcoins. In April, Taro, a technology that allows for the issuance of unique assets like stablecoins and NFTs was announced and at the end of September, the first alpha version was released. We are excited to see what the community builds around Taro as stablecoins and NFTs have become big use cases on other blockchains.

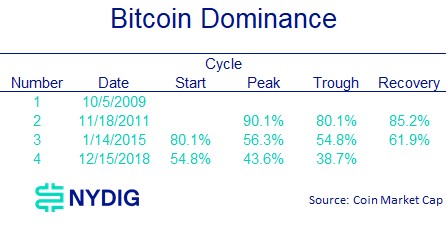

Bitcoin Historically has Gained Dominance During the Recovery Phase

There’s been quite a bit of discussion about bitcoin’s dominance, its share of the industry market cap, and its inability to take share during the recent drawdown. The data shows that historically, bitcoin has always lost dominance during the drawdown phase of a cycle. This happened in the second cycle from the peak in 2013 to the trough in 2015, the third cycle from the peak in 2017 to the trough in 2018, and it looks to be happening again in the current drawdown, which peaked in November 2021. Where bitcoin historically has gained dominance during the recovery phase, where bitcoin goes from a cyclical low back to its previous cycle high. In those times, bitcoin has always gained dominance. We can’t be certain that will happen again, but it is important to know that most of the darling coins of the previous cycle are unlikely to come back in a similar form. This happens every cycle, and bitcoin is one of the few digital assets with product-market fit.

Climbing a Wall of Worry to Find a Bottom

Investors continue to be plagued by fears in the market since the FTX fiasco. Unresolved questions about the fate of Genesis/DCG/Grayscale, the reserve status questions of exchanges such as Binance, Crypto.com, Huobi, and a host of others, and lingering questions about the state of other service providers run rampant. Our crystal ball is not any clearer on these matters than anyone else’s, however, it is important to note that we are already off over 75% from the price peak. Bad news, should it come, should be much less impactful to prices given where we are today.

The question on every investor’s mind has been, "when will bitcoin bottom?" It appeared to have done that throughout 3Q and much of 4Q after trading in a tight band for 5 months. Unfortunately, the events of 4Q jarred bitcoin loose from that range and sent it to a new cycle low. With some outstanding questions about the solvency of some important entities in the industry, such as Genesis and DCG, as well as concerns about the reserve status of some of the exchanges in the industry, investors continue to be on edge. If no new issues surface, a big if, it certainly seems like we have either hit a bottom or are near the bottom. Cyclical valuation indicators such as Market Cap to Realized Value (MVRV) point to a bottom forming and the price declines and duration of this drawdown are following a similar trajectory to the previous 3 drawdowns.

What will drive bitcoin higher? Having personally experienced the previous cycles, it was never obvious at the bottom either what the catalyst was. Perhaps it is that bitcoin is following an axis of growth and that its price temporarily over and then undershoots that trend, which accounts for these price cycles. Whatever the next catalyst is, Bitcoin is too important of technology to simply die or fade into obscurity. In the past, predicting Bitcoin’s demise has been hazardous to one’s wealth and that’s a rule we are confident will hold in the future.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication, the recipient acknowledges its understanding and acceptance of the foregoing terms.