What higher transaction fees mean for the health of the Bitcoin network.

This week marks the one-year anniversary of the LUNA-induced market crash. We look at the lasting impacts of those events.

With inflation cooling, we look at the upcoming macroeconomic events that could impact bitcoin.

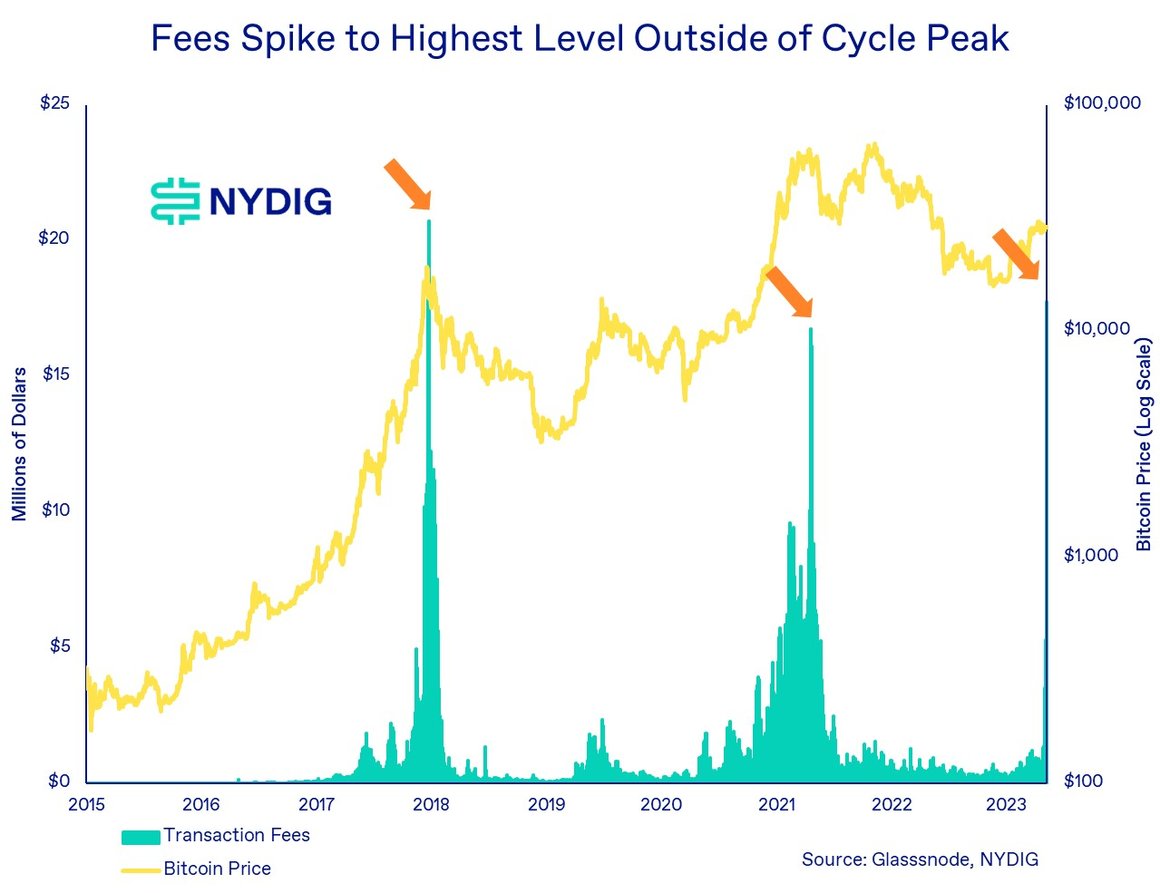

Spike in Network Activity Gives a Glimpse of Fee-Driven Future

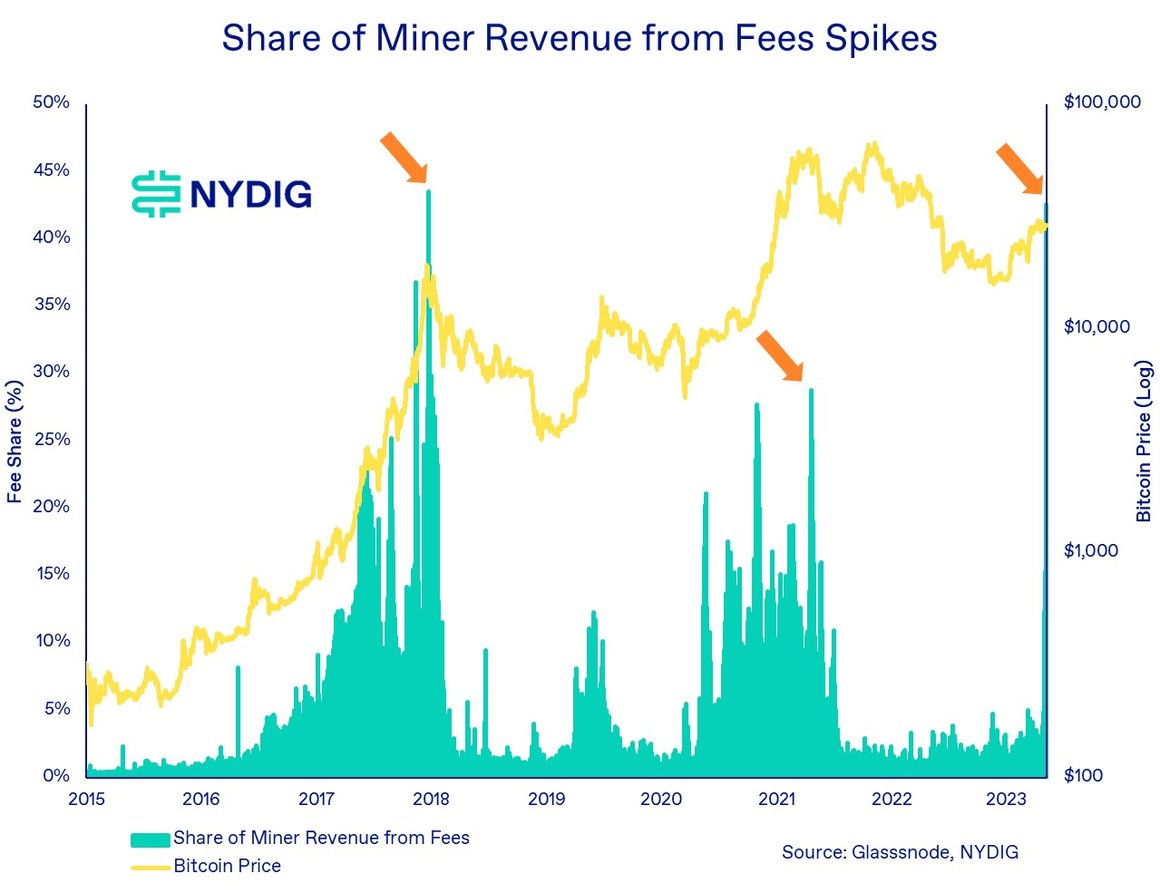

One of the important unanswered questions about Bitcoin’s future is how the blockchain will be secured when the supply of new bitcoins gradually dwindles to zero. Over the coming years, the security of Bitcoin, incentives paid to miners for their computational efforts, needs to transition from one mostly paid by the network itself via the block reward (new bitcoins) to one paid by its users (the senders of bitcoins) with transaction fees. The cost of network security, therefore, needs to transition from one born by the holders of bitcoins via dilution to one born by those engaging in on-chain activity. Until the rise of Ordinals and BRC-20s, the incentive for securing the Bitcoin network was heavily skewed to the block reward, accounting for the overwhelming majority of total miner revenue compared to transaction fees. However, with the explosion of on-chain activity driven by these new applications, the composition of miner rewards and fees has changed significantly, giving us a glimpse of what the future state of Bitcoin could be.

One crucial observation is that the inscription of Ordinals and BRC-20s caused the biggest spike in transaction fees outside of a cycle peak. It makes sense that high bitcoin prices also result in high transaction fees denominated in dollars, but transaction volume, or network activity, also appears to be largely positively correlated with price. As prices increase, users tend to send more transactions, moving funds around and creating more on-chain activity. The reverse is also true –when prices are depressed, network activity becomes subdued. The spike in fees driven by transaction activity outside of a cyclical price peak speaks to the growing utility of Bitcoin. Bitcoin’s use as a financial asset for investment purposes, one with high risk-adjusted returns and low correlations to other asset classes, has been far and away its biggest use case. But with the recent explosion of new applications rooted in Bitcoin, we see new behaviors emerge, ones that might lead to lasting uses for Bitcoin that could drive value.

The transition of Bitcoin’s “security model,” the composition of the compensation of miners, from bitcoins newly created by the protocol (the block reward) to transaction fees has long been an outstanding but unanswered question. While the extinguishment of the block reward is an eventuality baked into Bitcoin, there have been questions as to whether transaction fees would be sufficient to sustain adequate network security levels (hash rate). Until the launch of Ordinals in mid-January, transaction fees only accounted for 2%-3% of miner revenue, while the block reward accounted for most of their revenue, 97%-98%. Given this lopsidedness, it has been hard to imagine what a transaction fee-driven security model might look like. But now with the rise of Ordinals and BRC-20s, we glimpse what that future state may look like as transaction fees have jumped to over 40% of miner revenue, a level only seen in past cyclical price peaks. That future looks like significant demand for scarce block space supplied by Bitcoin’s blockchain, and transaction fees much higher than have been until recently driven by this demand.

It is not possible to predict the staying power of these new projects, but at a minimum, they’ve opened a new door to a new world of possibilities. We are excited to see where the entrepreneurial and technical energy takes us next.

Retrospective: Lessons Learned from the Collapse of LUNA/UST

This week marks the one-year anniversary of the collapse of the Terra (LUNA) platform and TerraUSD (UST) stable, which played a part in the failures of numerous fixtures within the digital asset ecosystem, including Three Arrows, Celsius, Voyager, Genesis, and BlockFi, just to name a few. The calamitous period last May was one of the seminal moments of the 2022 drawdown, perhaps only eclipsed by the collapse of FTX later in November. The industry is still grappling with the aftermath of these events, with bankruptcy proceedings underway, investor confidence shaken, market structure upended, and regulators out in force. While we cannot undo the events of 2022, our hope is that we can learn from them, and the industry can employ a more robust set of business practices to ensure this does not happen again. With the benefit of a year since the events, these are some of our most important takeaways.

Economic Design

At the heart of the failure of LUNA/UST was an unsustainable economic design, with the UST “stablecoin” supported only by the creation and destruction of the equity-like LUNA token. Without sufficient capital exogenous to the system (the money raised by the Luna Foundation Guard was insufficient) this design was flawed from the get-go and susceptible to the catastrophic risks it suffered.

Uneconomical Returns

While unsound economic design resulted in the unraveling of LUNA/UST, the interest rates paid by the Anchor Protocol (19.5%) to entice UST's creation were ultimately economically unsustainable. Instead of that yield being viewed as a source of guaranteed returns, it should have been eyed with extreme skepticism. While companies engage in uneconomical actions all the time, usually as short-term enticements, financial promises that appear too good to be true often are.

Counterparty Risk

A big takeaway from last year was proper counterparty risk assessment, whether it be to a centralized finance (CeFi) entity, like Three Arrows, or even a decentralized finance (DeFi) ecosystem like LUNA/UST. Aside from LUNA/UST, most of the counterparty risk had to do with CeFi players, like exchanges and lending platforms, and most DeFi applications held up well. Where DeFi applications held up less well, however, was in the security arena, where numerous hacks resulted in the theft of billions of dollars.

Arbitrage

“Arbitrage” is an overused term throughout much of crypto and one that is poorly applied. It is neither “riskless” in the academic sense nor involving the simultaneous purchase and sale of similar securities. Investors should be wary of its use because as we saw, these types of crypto “arbitrage” strategies often undertake significant risk.

Financial Pegs

Economic history is replete with examples of currencies that lost their pegs. To think that crypto assets are somehow different is to ignore much of the monetary history. While algorithmic stablecoins have been particularly problematic throughout the history of crypto, it is common to see collateralized stablecoins lose their peg simply because of market forces.

Decentralization

Just because an application is on a blockchain, does not mean it is decentralized in terms of control, operation, or ownership. Centralizing points of control can introduce points of failure, removing the trustless nature of this technology.

While these are certainly not the only lessons learned from the events of a year ago (personal attributes like humility come to mind), we think the community would be better served if some of these items were more prominent as we get ready for the next cycle.

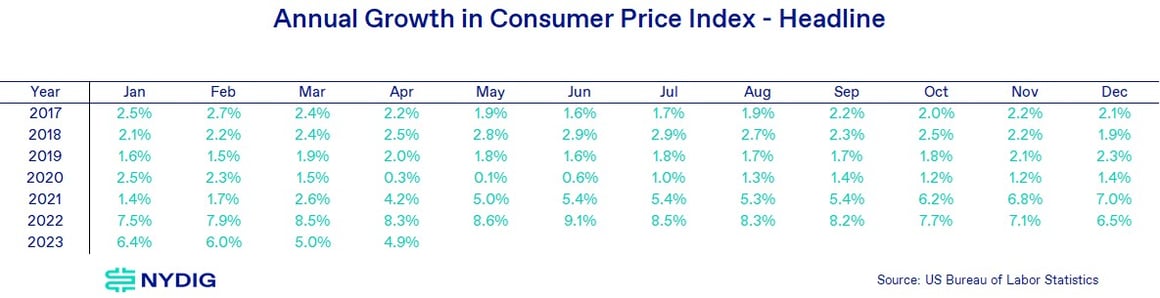

As Inflation Cools, What’s Next on the Macro Front?

This week the Bureau of Labor Statistics released the April Consumer Price Index (CPI), which showed a continued slowing of inflation. This continued slowing of inflation comes off the back of a year-plus-long rate rising campaign which also weighed on financial asset prices, such as stocks, bonds, and bitcoin, and could be seen as a cause of the regional banking crisis. While the battle against inflation might be far from over, our research shows that prior bouts of inflation were harder to quell than one might imagine, we wanted to look at what might be next on the economic front.

Interest Rates

The deceleration in inflation might give the Fed some breathing room on the interest rate front, which has been the main factor affecting asset prices over the past year. Forward rate expectations appear to have cooled off, with futures markets implying a 3.8% Fed Funds rate 12 months from now. Given the current FOMC target range of 5.0% - 5.25%, the market expectations of 3.8% 12 months from now imply that the Fed will embark on a rate-cutting campaign, just as it seems to be completing a rate-hiking campaign. While we do not profess to have a crystal ball regarding Fed rate decisions, our guess is that the direction of interest rates will likely be determined by other economic factors listed below.

Banking Crisis

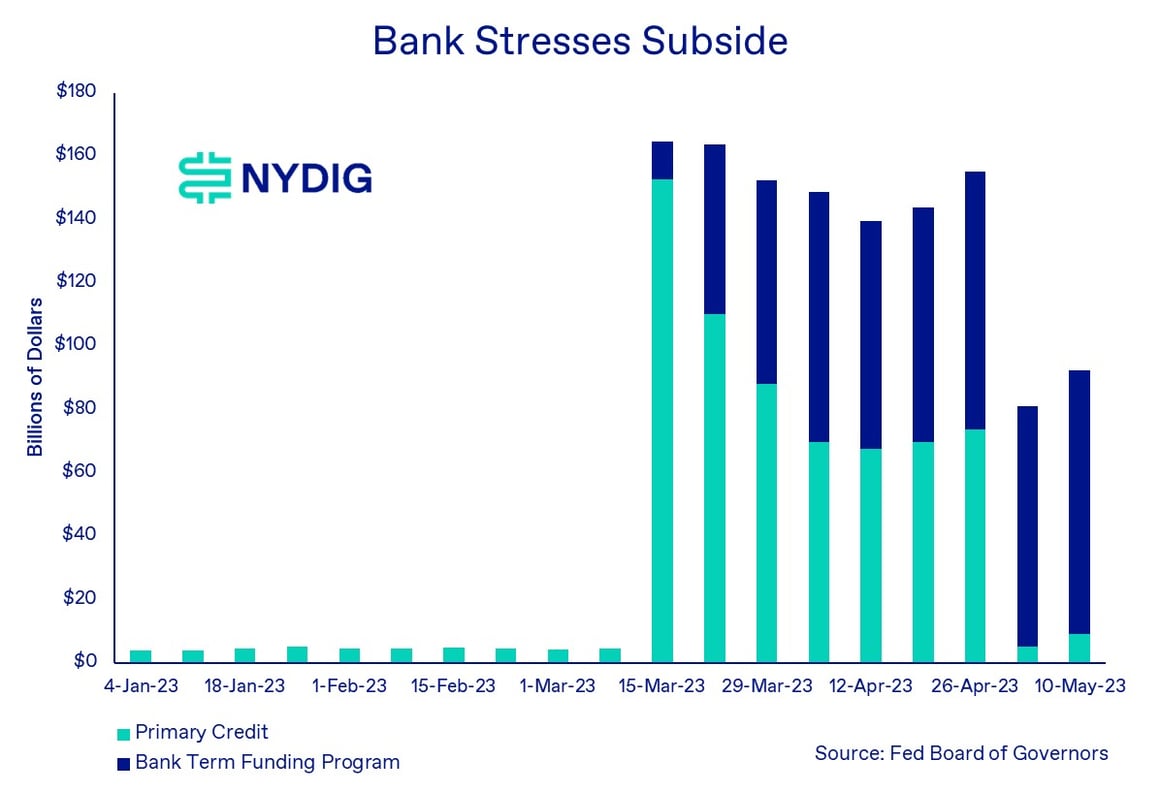

The regional banking crisis has been front and center throughout the year, shining a light on the need for an asset like bitcoin, one outside of the banking system. And while we have argued that bitcoin has been a beneficiary of the banking crisis, signs of banking system stress as measured by drawdowns on the Fed’s liquidity facilities like primary credit (the discount window) and the newly created Bank Term Funding Program (BTFP), have shown a cooling of the crisis. Our experience with banking crises is that they are rarely short-lived affairs, so while the situation is looking better at the moment, the root causes of built-up losses amidst rising rates have yet to be addressed fully. We think it would be premature to declare victory just yet.

Raising the Debt Ceiling

We covered this topic extensively a few weeks back, but it is worth a reminder as tensions seem to be ratcheting up amongst legislators with a possible deadline looming. This could be the most talked about macroeconomic item as we head into the summer months. Treasury Secretary Yellen continues to sound the alarm, as she did today in a Bloomberg interview, but ultimately it is up to legislators to sort out the situation. Bitcoin was relatively unknown during the contentious events of the 2011 debt ceiling negotiations but, given its prominence today, we wonder how it might act as a hedge to sovereign debt default risk. It is our opinion that non-sovereign issued stores of value like bitcoin and gold would do well in the event of that scenario.

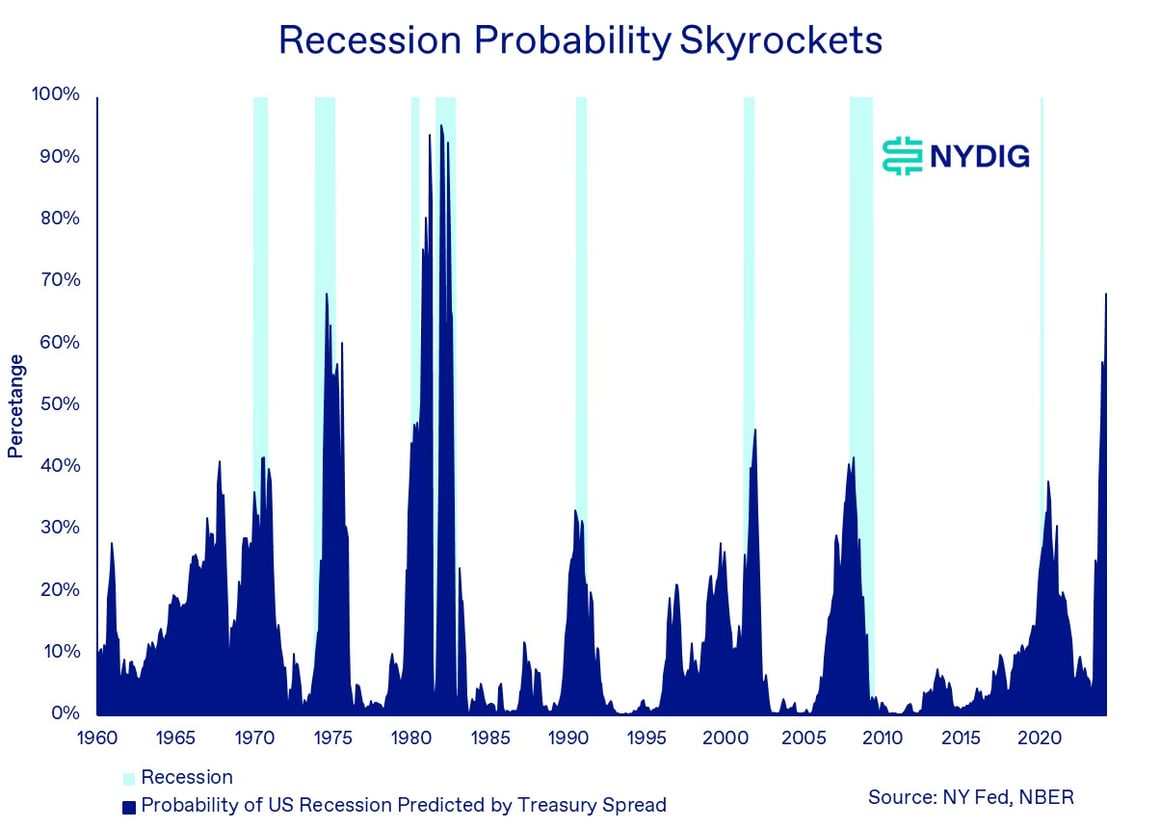

Recession Probability Skyrockets

We wrote about the prospects for a recession nearly a year ago, when the US experienced 2 consecutive quarters of declining GDP. While the cycle dating gurus refused to call that a recession, the probability of a recession in the next 12 months has skyrocketed to 68%, the highest level since the early 1980s. The probability model is based on the yield curve, whose inversions have historically been good bellwethers for recessions in the past. Recessions are inevitabilities of the economic cycle, and while predicting them is no easy feat, how markets and asset prices respond will likely be determined by the fiscal and monetary response to the slowdown. Risk assets are already well off their highs, so there is reason to believe that a recession might not be as deleterious to financial markets given that we have already come through a significant correction.

Market Update

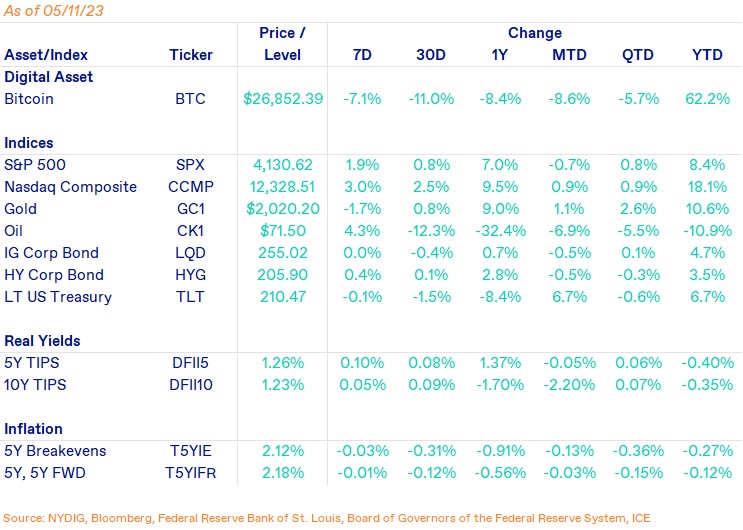

The price of bitcoin fell 7.1% as the asset continues to bounce about the upper $20Ks range. With the banking crisis cooling down, the ongoing regulatory overhang, and a lack of an immediate catalyst, investors have been taking profits after a meteoric rise since the beginning of the year. Equities rallied on the week with the S&P 500 up 1.9% and the Nasdaq Composite up 3.0%. Gold fell 1.7% on the week while oil bounced back 4.3%. Bonds were mixed on the week with investment grade bonds flat, high yield bonds up 0.4%, and long-term US Treasuries down 0.1%.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication, the recipient acknowledges its understanding and acceptance of the foregoing terms.