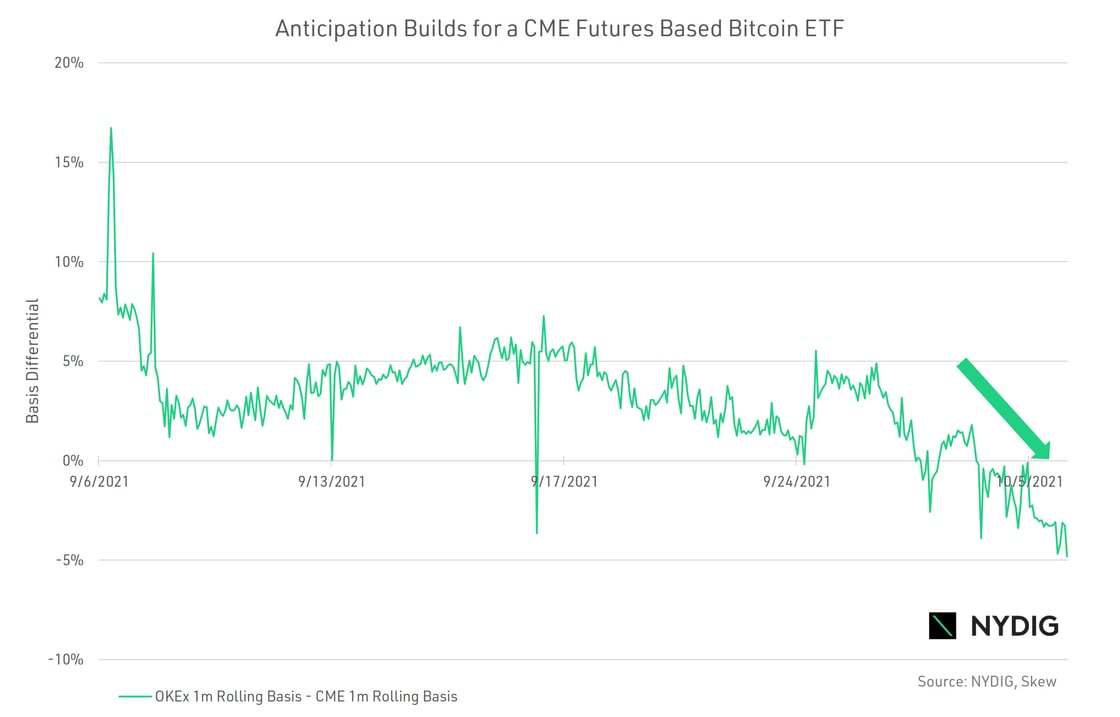

We see the growing basis premium for CME futures as a market signal of increased expectations for a futures backed ETF.

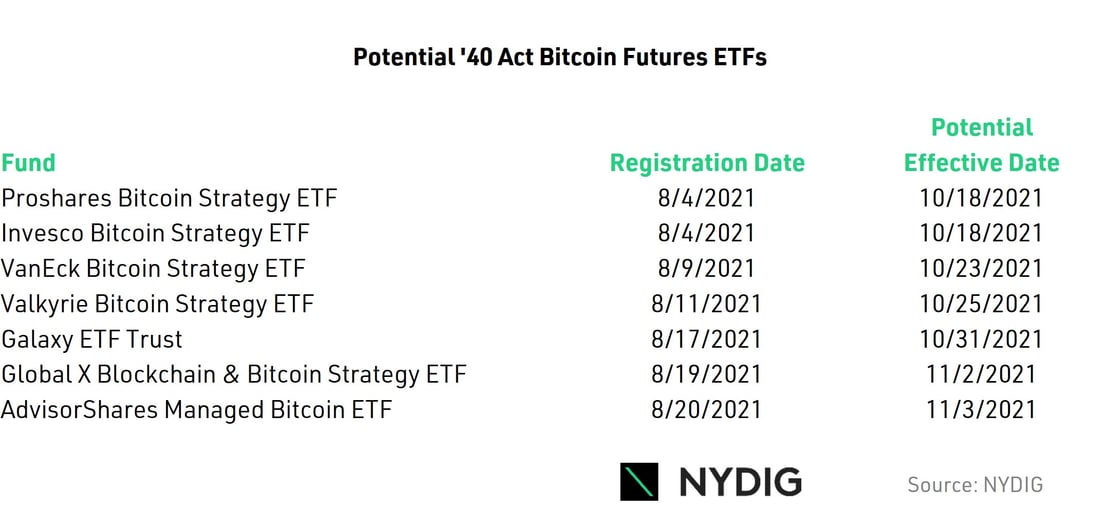

Although approval is not certain, Gensler has been supportive in recent comments. The first registration could be deemed effective on Oct 18th.

There are important implications, as well as drawbacks, to this type of ETF, including size limits, futures basis, price relative to NAV, deviations from spot price, the cost of implementation, and tax consequences.

Anticipation Builds for a Futures Backed Bitcoin ETF

Over the past few weeks, we have seen growing investor anticipation for a bitcoin futures ETF to finally begin trading on the CME. If this were to happen, this would complete a journey that first began in July 2013, with the filing of the Winklevoss Bitcoin Trust S-1 registration statement.

Signs of Optimism

We believe that the increasing basis for CME futures, the difference between futures and spot prices, is evidence of this investor optimism. The basis for CME futures has increased both on an absolute level and on a relative comparison with futures that trade on offshore derivative venues. The last time that CME futures registered a double-digit percentage annualized basis was in April when bitcoin was trading near its all-time high and the basis on offshore exchange OKEx was over 40%. Today the basis premium for futures traded on OKEx versus CME has flipped to a discount as CME futures are now trading at a basis premium for the first time.

SEC Signals Support of ’40 Act Futures-Based ETFs

On August 3rd, SEC Chairman Gary Gensler delivered prepared remarks at the Aspen Security Forum that first acknowledged the SEC’s public support for bitcoin ETFs registered under the Investment Company Act (’40 Act). Gensler’s remarks said “when combined with the other federal securities laws, the ’40 Act provides significant investor protections. Given these important protections, I look forward to the staff’s review of such filings, particularly if those are limited to these CME-traded Bitcoin futures.” A day later, on August 4th, registration statements were filed from Proshares and Invesco for ’40 Act bitcoin futures ETFs.

These filings differed from prior bitcoin ETF applications in that they sought to register under the ’40 Act, which is generally only available to funds that invest primarily in securities. Because a fund engaged in a bitcoin futures strategy will generally hold fixed-income securities as margin for the futures, such a fund can qualify to register under the ’40 Act. Prior bitcoin ETF applications were filed under the Securities Act of 1933 (’33 Act) because they will hold only bitcoin, which is not considered to be a security by the SEC, so they do not qualify for ’40 Act registration. NYDIG’s sister company, Stone Ridge Asset Management, pioneered bitcoin futures strategies in the ’40 Act, first in 2019 with the first-ever bitcoin futures fund in the ’40 Act (BTCNX) and followed in 2021 with the first-ever bitcoin futures mutual fund (BTCIX).

Limitations to Futures-Based Funds

An important distinction for investors between the new crop of ETF registrations and the prior applications is the mix of underlying investments. Prior applications relied mostly on owning spot bitcoin. In its denial of prior applications, the SEC has been concerned about the lack of investor protections on these trading venues and the potential for fraudulent and manipulative practices. New ETF registrations invest in bitcoin futures traded on CME, plus ETFs traded in Canada, open-ended investment products like the Grayscale Bitcoin Trust (GBTC), and publicly traded equities of digital asset-related companies, such as exchanges and miners.

Limits to Size. Bitcoin futures traded on CME do offer the investor protections the SEC is likely seeking, plus there is growing evidence of price formation and leadership for these products compared to spot. But because of the size of the futures market, ETFs may be limited in size or have unintended consequences on futures prices. On October 18th, the same day the first ETF may be deemed effective, the number of contracts that a participant such as an ETF can own is being raised to 6,000 in total, 4,000 for the front month and 2,000 for the second-month contract (there is usually very little open interest on the second-month contract). At 5 bitcoins per contract and $55,000 per bitcoin, that limits the size of an ETF to $1.65B in AUM. While that may seem small in comparison to the $34.2B Grayscale Bitcoin Trust (GBTC), the notional total open interest on CME futures is only $2.8B. Given there are 7 bitcoin futures ETFs we are tracking, that amounts to potential incremental total open interest of $11.6B from these new funds. Given the size of the potential increase of open interest compared to the current open interest, approvals of futures-based ETFs are likely to have a meaningful impact on the price of futures and therefore the basis.

Size Limits May Impact Premium to NAV. ETFs are open-ended investment vehicles that create and redeem shares throughout the trading day. The small size of a bitcoin futures ETF, or at least the portion of these funds allocated to bitcoin futures, may result in some unintended consequences. If the contract size limit is reached, a fund may not be able to create new shares for purchasers. As a result, new share creation may be suspended. Also, because a fund cannot limit the secondary market trading of its shares, the shares of the ETF may trade at a significant premium to its Net Asset Value, which has caused performance issues relative to the price of bitcoin for vehicles, such as GBTC, if the premium collapses or flips to a discount.

Alternative Investments Introduce New Risks, Increase Tracking Error to Bitcoin. Most of the new crop of ETF registration statements propose that the funds may invest in other instruments besides bitcoin futures. These investments include bitcoin ecosystem equities, such as miners and exchanges, ETFs listed outside of the US, and open-ended private trusts such as the Grayscale Bitcoin Trust. These investments introduce completely new risks and increase the tracking error to the price of bitcoin.

Futures Roll Could Prove to be Costly. The bitcoin futures curve is typically in contango, meaning it has an upwards slope - successive month futures trade at increasingly higher prices. This means that as a fund “rolls” futures from one month to the next, it sells the expiring contracts and purchases the next month’s contracts. This creates costs for investors in these funds. Our estimate of the historical cost of rolling futures is 4% - 6% annually, but these costs could increase meaningfully if the futures basis continues to increase. These are costs that could affect returns for investors that own one of these funds versus owning spot bitcoin.

Important Tax Consequences. There are important tax consequences that arise from futures-based funds. For example, the gains on futures rolled every month would be realized every year for investors and taxed as ordinary income instead of being deferred and potentially realized as long-term capital gains. Furthermore, capital losses are “trapped” within the fund. If the fund has a down year, investors cannot net off the futures losses against other investments. Losses are carried forward within the fund to be deducted against future bitcoin futures gains.

We note that the same arguments that that SEC will need to weigh in considering a futures-based bitcoin ETF – specifically the growth of the futures market and the fact that significant price discovery occurs in the futures market – also give the SEC grounds under their rules and previous statements to approve an ETF that holds spot bitcoin instead of bitcoin futures. We continue to believe that such an ETF would be preferable for investors, for the reasons outlined above, and would be more resilient to manipulation given the depth and liquidity of both the futures spot and bitcoin markets.

Implications of an Approval

While the investment strategies differ by fund, some broad-based takeaways are likely to hold if these registration statements are deemed effective.

Basis Could Rise. Meaningfully. We pointed out earlier that the basis for bitcoin futures traded on the CME had risen to levels not seen since April. If an ETF were to begin trading, incremental demand for futures could push the basis up even higher. Given the differential between the current total open interest of $2.8B and the potential total demand of $11.6B created by the 7 ETFs, the impact on the basis could be significant.

Incremental Demand for Canadian ETFs. Many of the registration statements provide for the purchase of ETFs that trade on exchanges in other countries, most notably Canada. These funds, almost all of which exclusively own spot bitcoin, could see incremental demand.

Impact on GBTC is Hard to Predict. This item is a little more difficult to predict. On one hand, the presence of a US-traded alternative to GBTC represents a competitive threat to the massive investment trust. The discount to NAV could widen based on that view. But on the other hand, the discount in the price of GBTC to its NAV of -17.2% already reflects a healthy dose of competition, one first brought on by the appearance of the Canadian ETFs in February. The fact that some of these new ETFs could buy GBTC may narrow the discount.

Does a Bitcoin ETF Even Matter?

Without a doubt, the importance of a US-based ETF has lessened since it was first proposed in 2013. Today, there is a myriad of ways for institutional and retail investors to get exposure to bitcoin. While the symbolic nature of a bitcoin ETF traded on a US-based exchange is important, especially after years of failed attempts, the form that these vehicles take, based on bitcoin futures, is less than ideal. Nonetheless, we would expect the price to react positively to the news of an ETF, with the first of these funds potentially becoming effective in just a few weeks.

Market Update

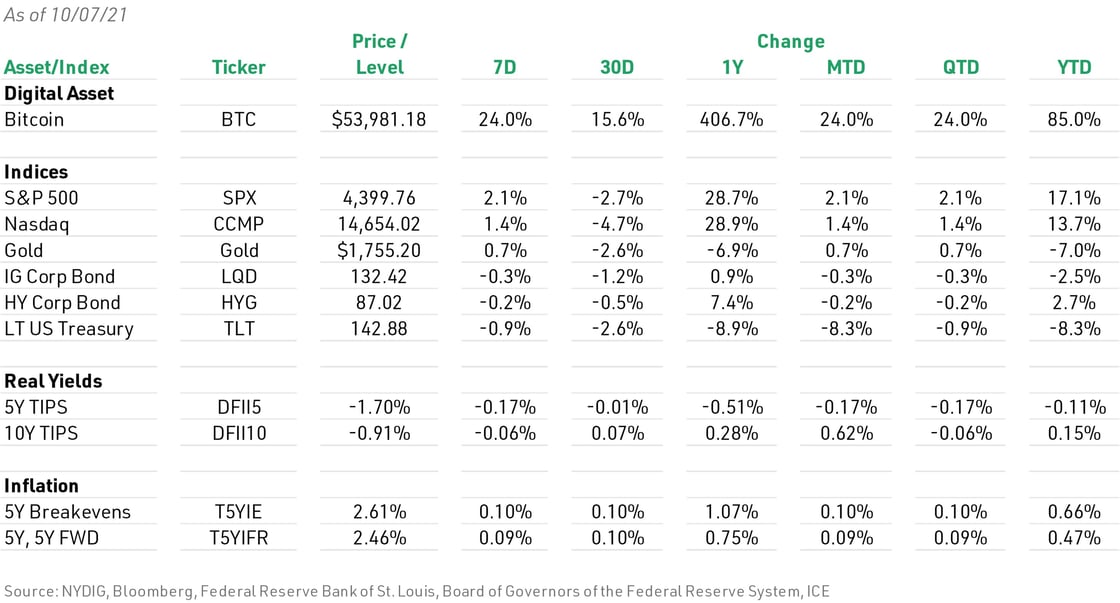

Bitcoin had a very strong week, up +24.0%, as investors’ fears about an onerous regulatory environment faded and enthusiasm for a bitcoin futures ETF emerged. Equities had a strong week as well, with the S&P 500 up 2.1% and Nasdaq Composite up 1.4%. Against this risk-on backdrop, bonds fell, with Investment Grade Corporate Bonds down -0.3%, High Yield Corporate Bonds down 0.2%, and Long-Term US Treasuries down -0.9%. Gold was up +0.7% on the week as inflation expectations rose and real yields fell.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication in its entirety, the recipient acknowledges its understanding and acceptance of the foregoing terms.