• A look at innovations sparked by digital scarcity

• Today’s options expiry had traders guessing

• Redefining the notion of public and private money

Digital Scarcity in the Time of Bitcoin

The concept of “digital scarcity,” the idea that digital resources such as software programs and electronic files could be made to be limited despite being infinitely replicable at zero marginal cost, traces its roots back to the early 2000s. This was well before the advent of Bitcoin and at a time when the hot button issue was music file sharing through peer-to-peer applications, such as Napster, Kazaa, and LimeWire. At the time, the focus was on the enforcement of the Digital Millennium Copyright Act (DMCA), the 1998 law that criminalized the possession and dissemination of copyrighted works, through a process called Digital Rights Management (DRM). DRM was the enforcement of digital scarcity and user control through a process of verification, encryption, and tracking. This era and style of digital scarcity, one still predominantly in use today, can be described as top-down, driven by the employment of technology and business processes to enforce our nation’s laws.

The creation of Bitcoin turned the idea of digital scarcity on its head. Digital scarcity permeates the technology and comes from the ground up, from the fidelity of bitcoin ownership through a chain of digital signatures to the rules-based supply function that limits the supply of the asset. Bitcoin creates digital scarcity not through legal edict and business processes but rather through technical innovation. The power of its network is its open, opt-in nature that attracts users not because they are forced to, but because they choose to.

Today, over 12 years after Bitcoin’s genesis block, the Big Bang in crypto has spewed forth digital scarcity across the industry like cosmic dust. It coalesces in the over 11,000 digital assets in the ecosystem, each one an experiment in economic policy, technology design, and use cases. We see digital scarcity in the current Non-Fungible Token (NFT) boom, a trend that has been underway throughout 2021. While we have no opinion on the value of any single NFT (after all, the value of art is the ultimate exercise in subjectivity), we think the value that digital scarcity unlocks for the creative class is powerful. While we currently believe the biggest use case for digital scarcity will likely be money, the transition to digital goods in the virtual world is an undeniable secular trend. As these applications of digital scarcity continue to evolve, it’s important to remember that they are all possible because of the innovations brought together by Bitcoin.

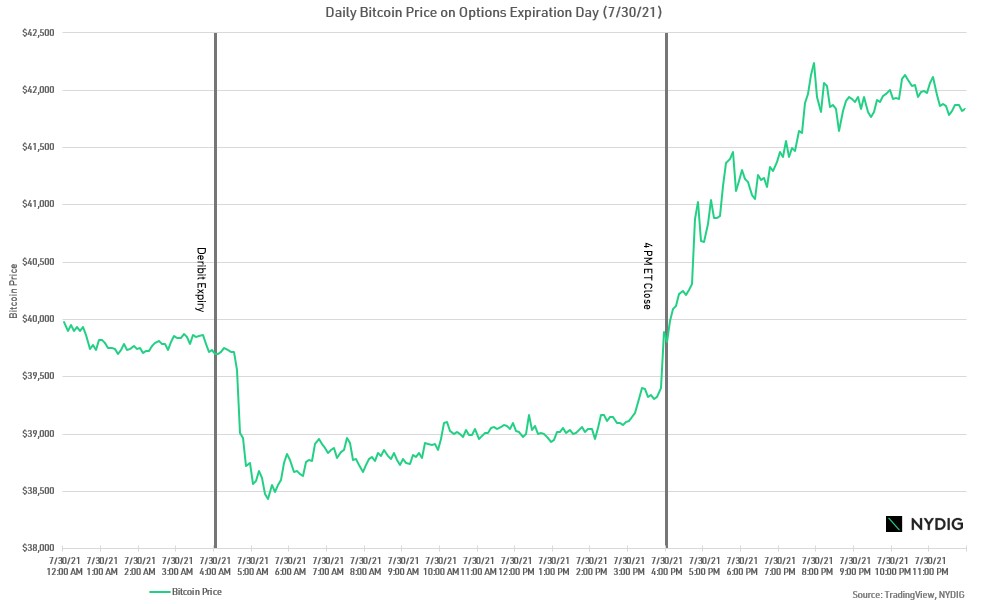

Options Expirations Impact Difficult to Predict

By the time this weekly newsletter hits your inboxes, the monthly expiration of bitcoin futures and options will have just passed. There are two important windows for active investors: the Deribit expiration, which occurs at 8 am UTC (currently 4 am ET), and the CME expiration, which occurs at 4 pm London (currently 11 am ET). The Deribit window is arguably more consequential because, as an exchange, Deribit regularly trades more than 90% of the daily options volume across the market.

It seems like every month as we get towards the expiration date, the crypto media likes to point out the notional size of the options that are set to expire. While this number is an interesting data point, the impact of expiration on the price of spot bitcoin is difficult to determine. While we have certainly noticed some interesting price behavior around expiration historically, it is difficult to predict the price action ahead of time, purely because we do not know how dealers are positioned or their propensity to delta hedge. Last month in particular saw some interesting price action right after expiry, as the price of bitcoin fell over 3% in a 15-minute time frame. The price of spot bitcoin then steadily rose throughout the day and jumped after the 4 pm ET close, a dynamic that likely had to do with monthly subscriptions to bitcoin funds. While these price movements can be explained after the fact, predicting price action ahead of time is difficult given we do not know key pieces of information, such as dealer positioning and fund subscriptions or redemptions.

Bitcoin: Public or Private Money?

Three weeks ago, at the Aspen Security Forum, SEC Chairman Gary Gensler referred to Bitcoin as a ”private form of money with no central intermediary, such as a central bank or commercial banks.” While it is true that bitcoin is not a “public money” in the traditional sense, one issued by a nation state’s central bank, to us, Bitcoin is anything but private. Bitcoin’s open-source nature makes it freely available for anyone to use, a supranational currency that transcends geographic border available to anyone with a smartphone or computer and an internet connection. Download Bitcoin for use here, participate in technical development on GitHub here, contribute to development discussions on the mailing list here, engage on the message boards here, and join in online chats here. Try doing something like that with “public money.”

Market Overview

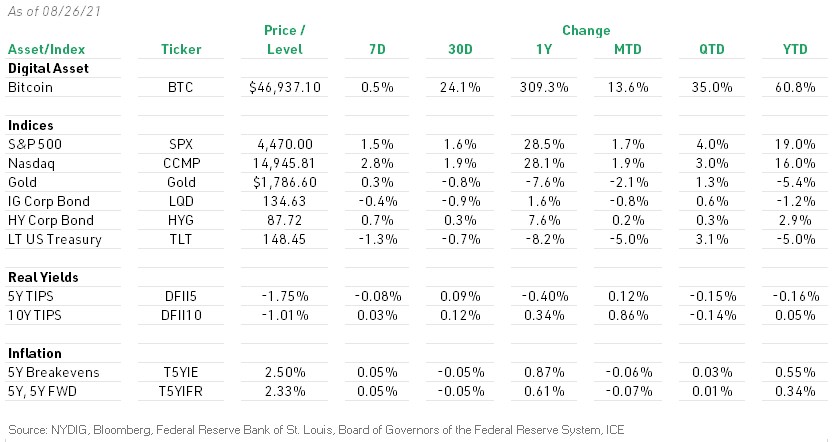

Bitcoin continued to bounce back from the mid-summer sell-off, breaking above $50K briefly on Monday, a price level it had not seen since mid-May. Unfortunately, despite piercing $50K, bitcoin was unable to hold that level for long as traders seized the +75% rally from the trough to take profits. Traders are now eying the 200-day moving average of $46,500 as a level of support. Investors had an appetite for risk this week as equities had a strong week with the S&P 500 up 1.5% and the Nasdaq Composite up 2.8%. Bonds were down except for high-yield bonds. Investment-grade corporate bonds were down 0.4%, high-yield corporate bonds were up 0.7%, and long-term US treasuries were down 1.3%. Gold was up 0.3%, as inflation expectations ticked up slightly and real yields were mixed.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication in its entirety, the recipient acknowledges its understanding and acceptance of the foregoing terms.