We review the controversial status of the U.S. economy and what it means for markets

As the Fed hikes, market expectations are telling a different story about future interest rates

Traders are still undecided about bitcoin prices

Recession: What’s in a Name?

The U.S. Department of Commerce announced yesterday that real GDP had contracted by an annual rate of 0.9% in Q2 2022, following a decrease of 1.6% annualized in Q1 2022. Despite the contraction, markets rallied on the news, as investors had expected worse, but the news sparked a debate over whether the economy is in a recession. Given that bitcoin has been trading as a risk asset this year, the state of the economy is worth reviewing.

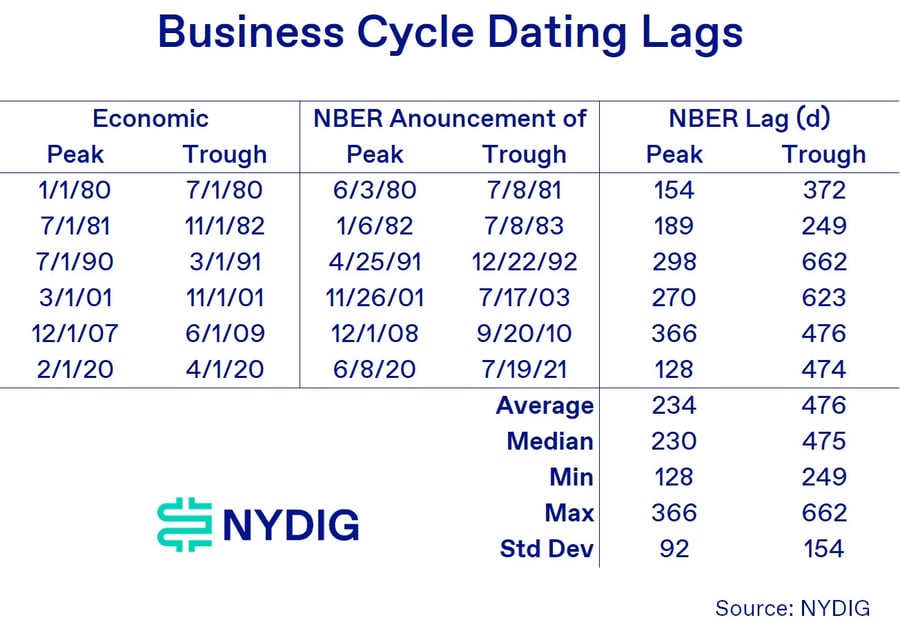

By one very common definition of a recession — two consecutive quarters of negative economic growth — the United States is currently in one. However, the White House and the Federal Reserve have pushed back against this notion, instead pointing to the economic cycle dating efforts put forth by the National Bureau of Economic Research (NBER), a private, non-profit organization devoted to disseminating economic research. The NBER’s definition of a recession, which can be found here, allows for much more subjectivity in dating economic expansions and contractions. The “two quarters” rule, while very widespread, dates back to an article originally published in the New York Times in 1971 by Commissioner of the Bureau of Labor Statistics Julius Shiskin, in which it is presented as one of three potential rules of thumb for determining a recession. While NBER allows for more subjectivity in its definition, interestingly, since the NBER started dating recessions in 1980, there have never been two consecutive quarters of real GDP decline that have not been subsequently deemed as part of a recession. In fact, of the six recessions that have taken place in this period, only one (the dot-com bubble burst in 2000) did not have two consecutive quarters of GDP decline, suggesting that the “two quarter” rule has been a decent indicator of recessions in the past.

Quibbles over precise definitions of economic terms aside, the NBER is very late in identifying economic inflection points - cycle peaks and troughs. On average, the NBER announcement of economic peaks have come 234 days after the economic peak, and the announcement of economic troughs have come 476 days after the economic trough. Investors should understand that the recognition of an economic inflection point is very much a backward-looking event.

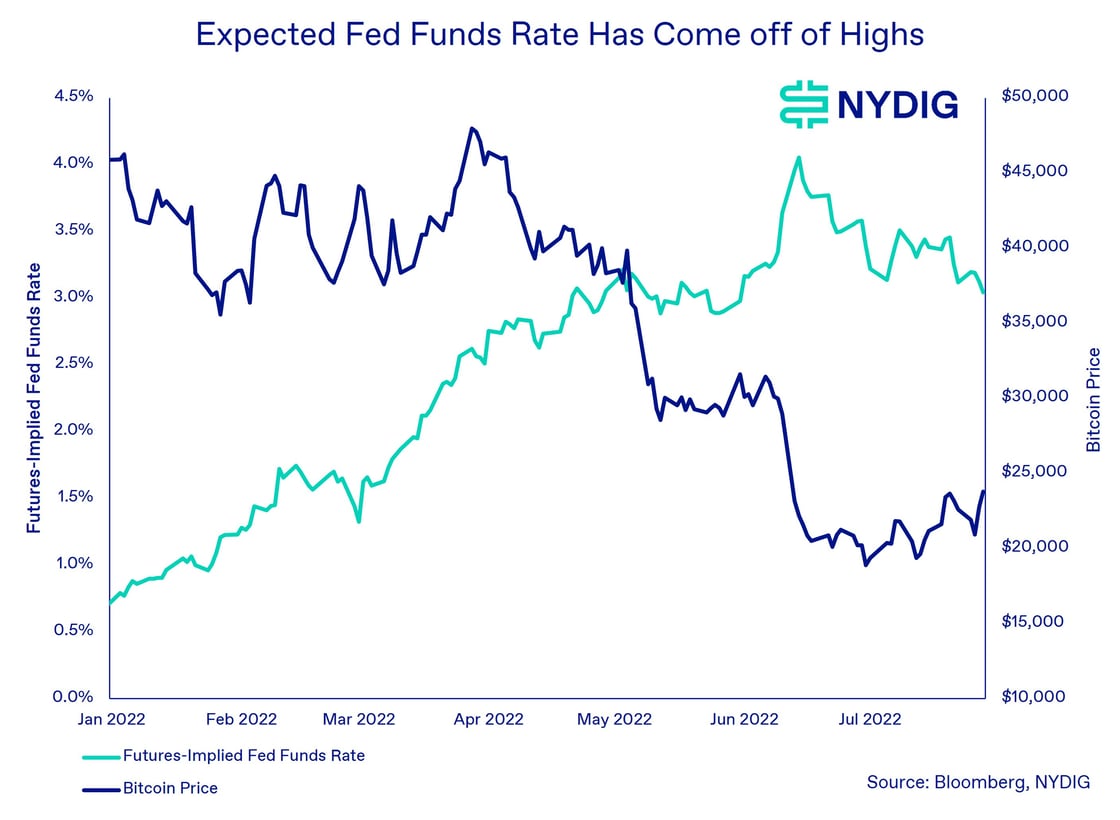

The Fed Raises Rates While Market Expectations Cool

On Wednesday, the Fed announced that it would be raising its benchmark overnight borrowing rate by 75bps up to a range of 2.25% - 2.50%. The hike was priced well in advance, and in fact, there was a small probability of a 100bps hike priced into markets. As a result, markets jumped on the news, with the S&P 500 ending the day up 2.6% and bitcoin up 8.9%.

Despite the fact the Fed continues to hike, market-based expectations for interest rates 12 months into the future, based on Fed Funds Futures, continue to decline. Last month, these futures predicted that the overnight rate would be as high as 4.0% in a year’s time. That level has decreased to 3.0%. Investors, it seems, are growing less fearful of an aggressive hiking path. With bitcoin following the contours of Fed expectations this year, this may be one of the causes of the recent price rally.

Traders Still on the Sidelines Despite Recent Price Bump

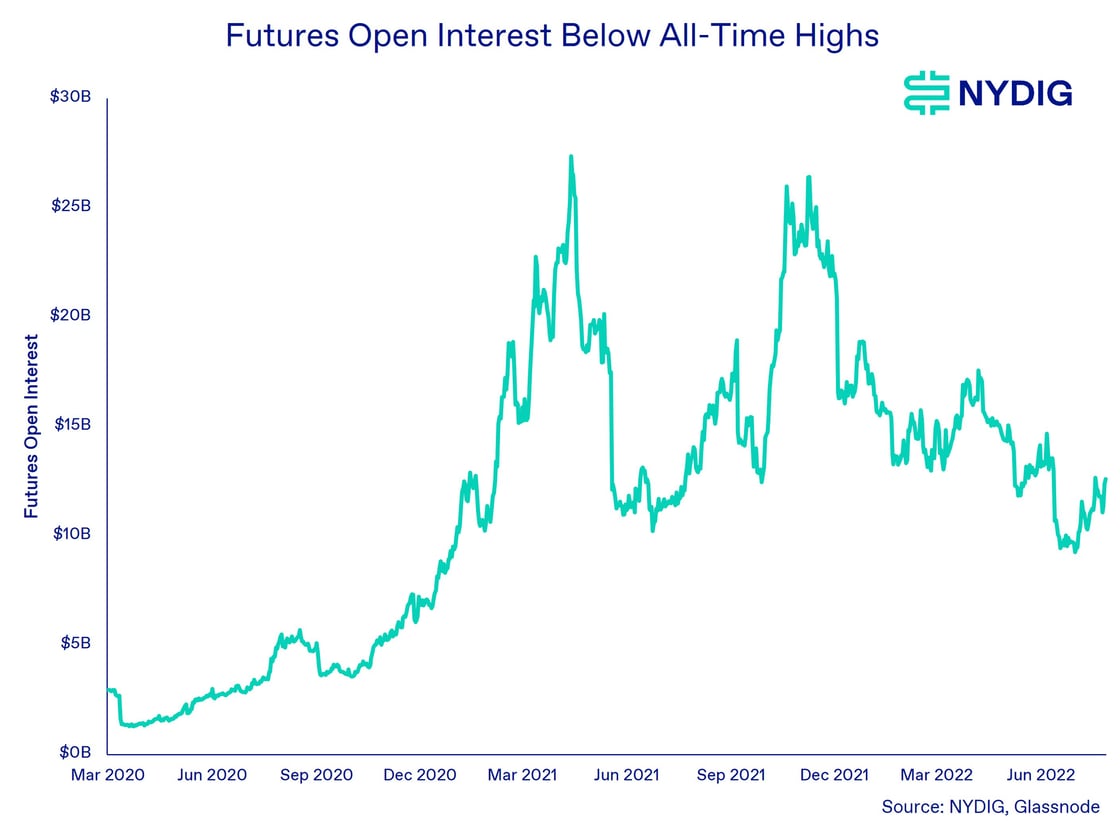

Even though bitcoin is up 35.5% off its recent $17,567 lows, market data continues to show that traders are conservatively positioned. Open interest in futures and options remains well below all-time highs, and perpetual swap funding rates indicate little directionality.

Futures open interest presently stands at $12.5B, up off the recent lows but still well below all-time highs of $27.43 last year. Futures open interest on measured exchanges (Binance, Bitfinex, Bitmex, Bybit, CME, Deribit, FTX, Huobi, Kraken, OKX) has been on a downward trend since the November launch of the ProShares Bitcoin Strategy ETF (BITO), which invests in bitcoin futures traded on the Chicago Mercantile Exchange (CME). We think the downward trend in open interest is reflective of investor sentiment in the asset over the past 9 months and, while we are encouraged that it is up off the recent lows, it does not provide sufficient evidence to us that investor mentality has shifted.

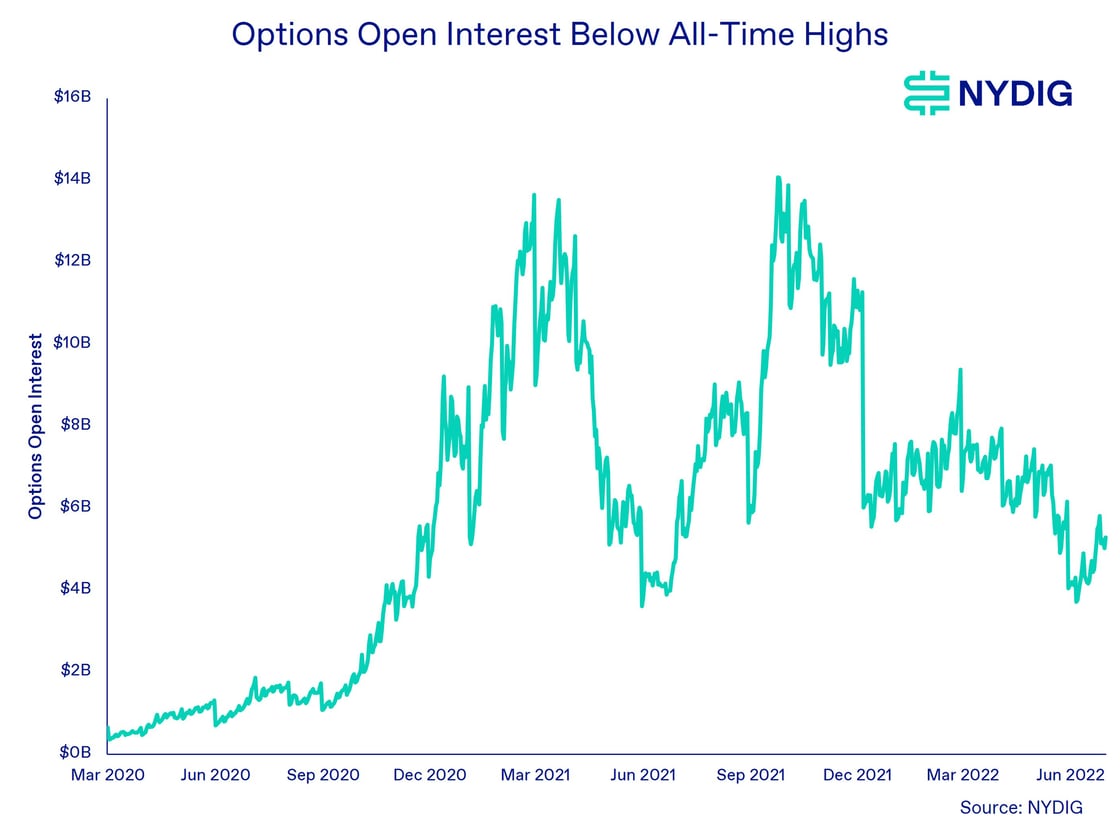

Open interest in options on Deribit tells a similar story to that of futures, also on a downward trend over the past 9 months but with signs of coming off the recent lows. Options traders appear to be expressing similar attitudes as futures traders.

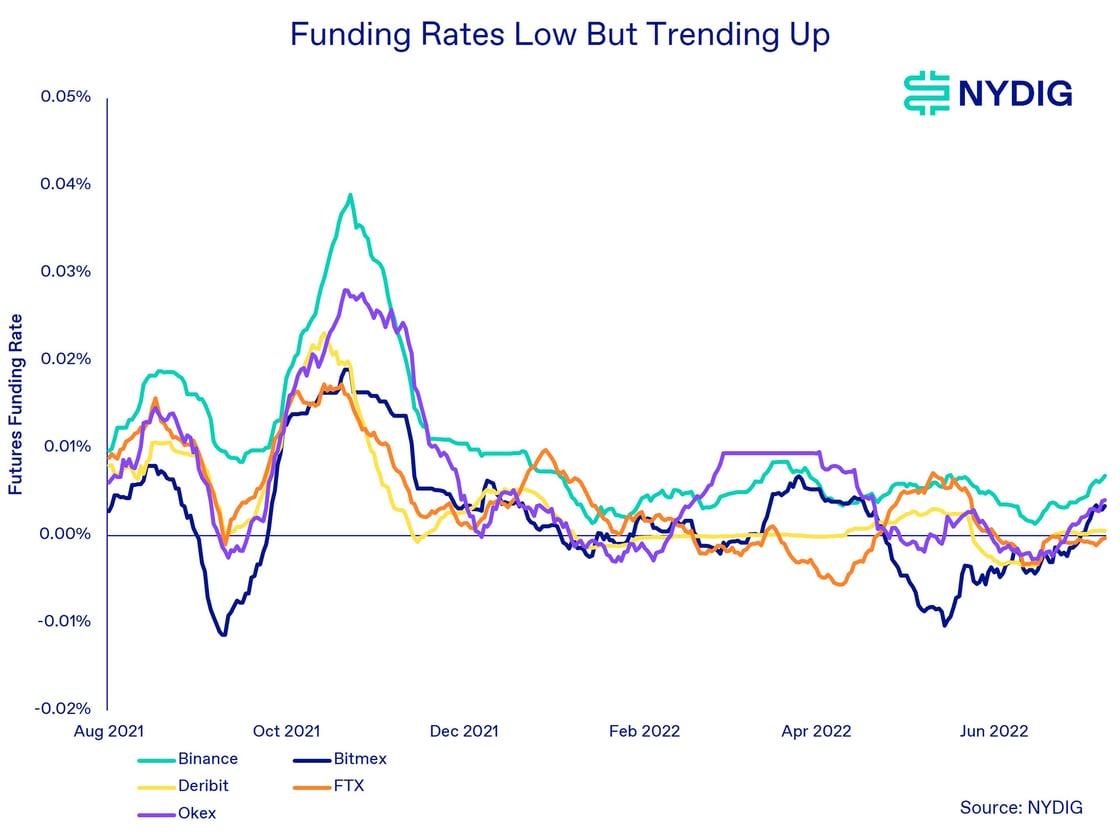

Funding rates on perpetual swaps, the market-based interest paid by traders taking out long and short positions, are also up off the lows but remain at muted levels. Positive funding rates indicate that traders are willing to pay up to take levered long positions, implying bullish positioning. The fact that funding rates are still low on an absolute basis indicates a lack of desire for traders to take directional bets, though they do appear to be trending higher.

Market Update

Risky assets continued to rally this week. Bitcoin gained 2.6%, while the S&P 500 gained 1.9%, and the Nasdaq appreciated 0.9%. Bonds also gained: Investment Grade Corporate Bonds were up 1.4%, High Yield Corporate Bonds appreciated by 1.3%, and Long-Term Treasuries gained 1.0%. Gold increased by 2.8% on the week as real yields decreased and inflation expectations increased.

You are receiving this email because you signed up to receive our weekly research at www.nydig.com

This communication has been prepared solely for informational purposes and does not represent investment advice or provide an opinion regarding the fairness of any transaction to any and all parties nor does it constitute an offer, solicitation or a recommendation to buy or sell any particular security or instrument or to adopt any investment strategy. Charts and graphs provided herein are for illustrative purposes only. This communication does not represent valuation judgments with respect to any financial instrument, issuer, security or sector that may be described or referenced herein and does not represent a formal or official view of New York Digital Investment Group or its affiliates (collectively NYDIG).

It should not be assumed that NYDIG will make investment recommendations in the future that are consistent with the views expressed herein, or use any or all of the techniques or methods of analysis described herein. NYDIG may have positions (long or short) or engage in securities transactions that are not consistent with the information and views expressed in this communication.

The information provided herein is valid only for the purpose stated herein and as of the date hereof (or such other date as may be indicated herein) and no undertaking has been made to update the information, which may be superseded by subsequent market events or for other reasons. The information in this communication may contain forward-looking statements regarding future events, targets or expectations. NYDIG neither assumes any duty to nor undertakes to update any forward-looking statements. There is no assurance that any forward-looking events or targets will be achieved, and actual outcomes may be significantly different from those shown herein. The information in this communication, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Information furnished by others, upon which all or portions of this communication are based, are from sources believed to be reliable. However, NYDIG makes no representation as to the accuracy, adequacy or completeness of such information and has accepted the information without further verification. No warranty is given as to the accuracy, adequacy or completeness of such information. No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this communication to reflect changes, events or conditions that occur subsequent to the date hereof.

Nothing contained herein constitutes investment, legal, tax or other advice nor is it to be relied on in making an investment or other decision. Legal advice can only be provided by legal counsel. NYDIG shall have no liability to any third party in respect of this communication or any actions taken or decisions made as a consequence of the information set forth herein. By accepting this communication, the recipient acknowledges its understanding and acceptance of the foregoing terms.